This report is issued by and on behalf of altshare Ltd. ("altshare") for informational purposes only and shall not be construed as legal, financial, or tax advice.

The information contained in this report is based on data provided to and/or prepared by altshare for its clients. The report is based on an aggregated and anonymized data from altshare's clients.

While this report may address potential legal, financial, and/or tax matters, it does not constitute professional advice in these areas. The opinions or conclusions expressed herein are not to be attributed to altshare. We strongly recommend that you seek the counsel of qualified advisors before taking any actions based on the information provided in this report.

For the avoidance of doubt, altshare shall not assume any liability for, nor be held responsible for any damages, losses, claims, or expenses, whether direct, indirect, incidental, consequential, special, or punitive, arising from the use or reliance on the information contained in this report. altshare shall not be liable for any actions taken or not taken based on the information contained herein.

altshare does not warrant the accuracy, completeness, or reliability of the data presented and assumes no responsibility for any errors or omissions. The information provided in this report is subject to change without notice.

This report is provided "as is" and altshare disclaims any responsibility for the outcomes of decisions made by the recipient or any third party in reliance on its contents.

• Seed Rounds by Sector

• Series A Rounds by Sector

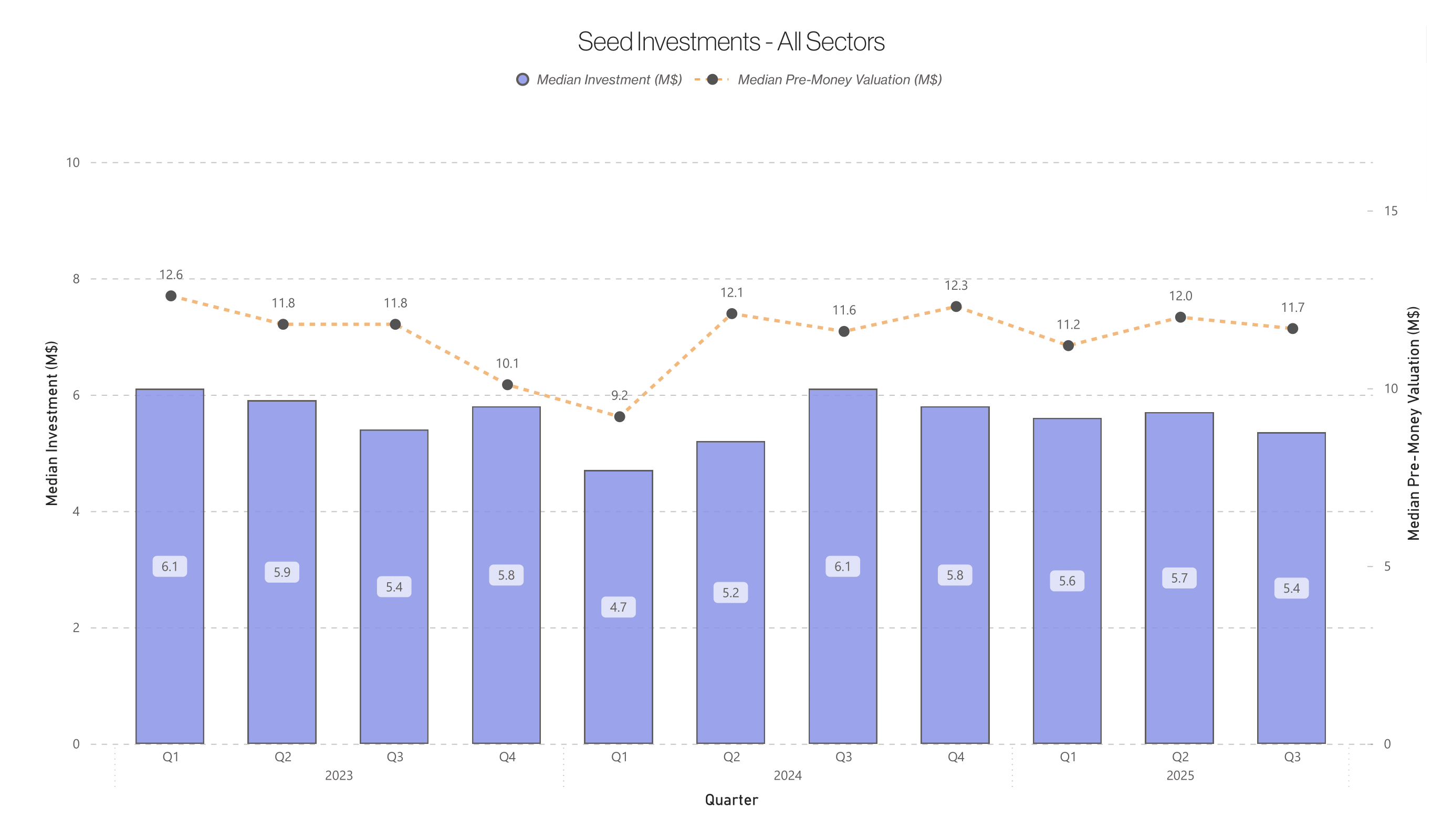

Seed funding across all sectors continues to find its balance. In Q3 2025, the median seed round reached $5.4M, with a $11.7M median pre-money, signaling a market that’s steady, selective, and focused on quality over hype.

Seed funding in AI & Data-Driven Technologies continues to gain momentum. In Q3 2025, the median round reached $5.8M, with a $15.5M median pre-money valuation, reflecting renewed investor confidence in data-driven innovation.

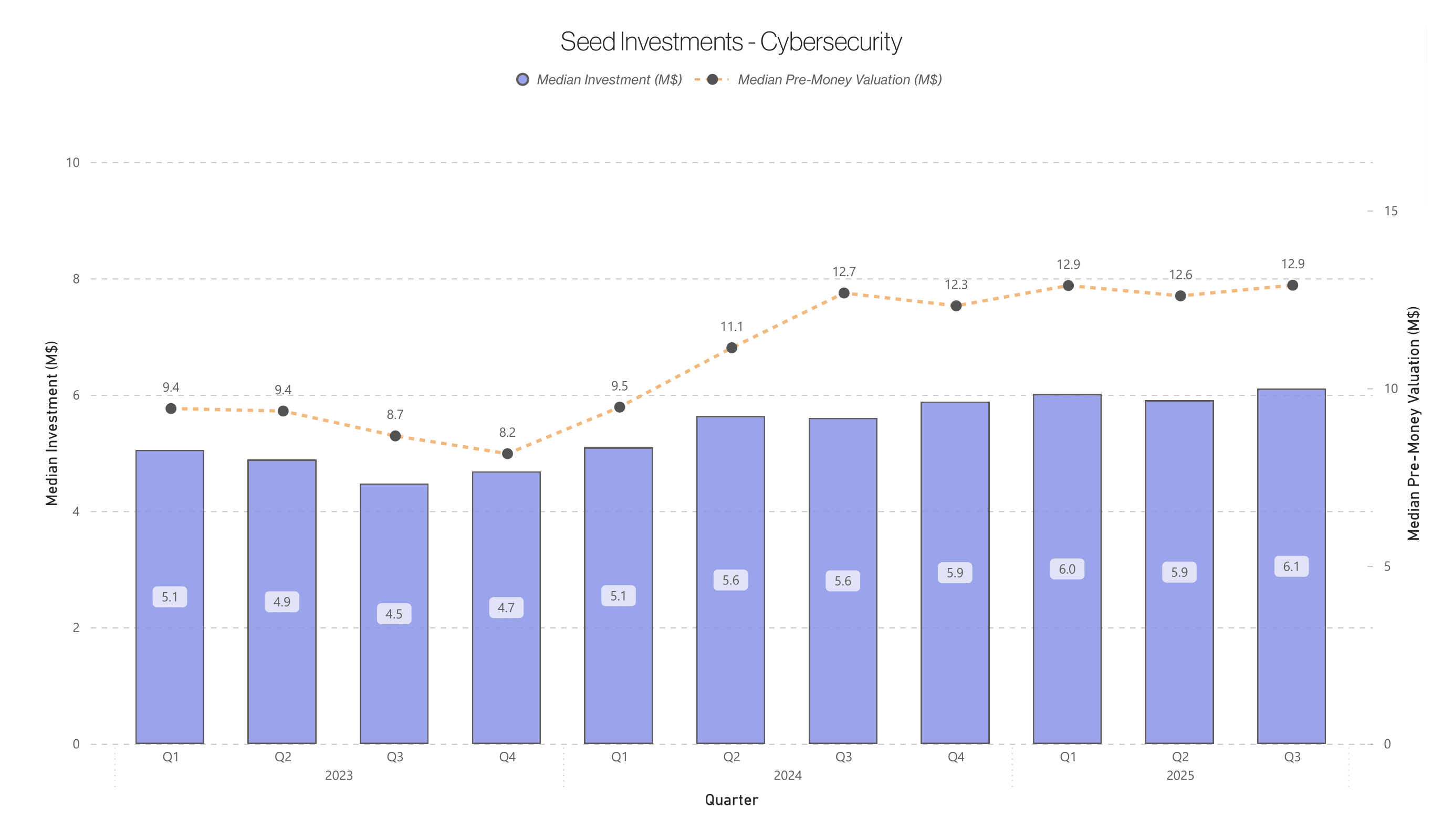

Seed funding in Cybersecurity continues on a steady upward path. In Q3 2025, the median seed investment reached $6.1M, with a $12.9M median pre-money, underscoring ongoing investor confidence in the sector’s resilience and growth potential.

Seed funding in HealthTech cooled slightly this quarter. The median investment landed at $2.6M, with a $7.6M median pre-money valuation. Compared to Q3 2024, investments are smaller, but valuations remain higher, pointing to a market that’s recalibrating after a strong start to the year and prioritizing quality over pace.

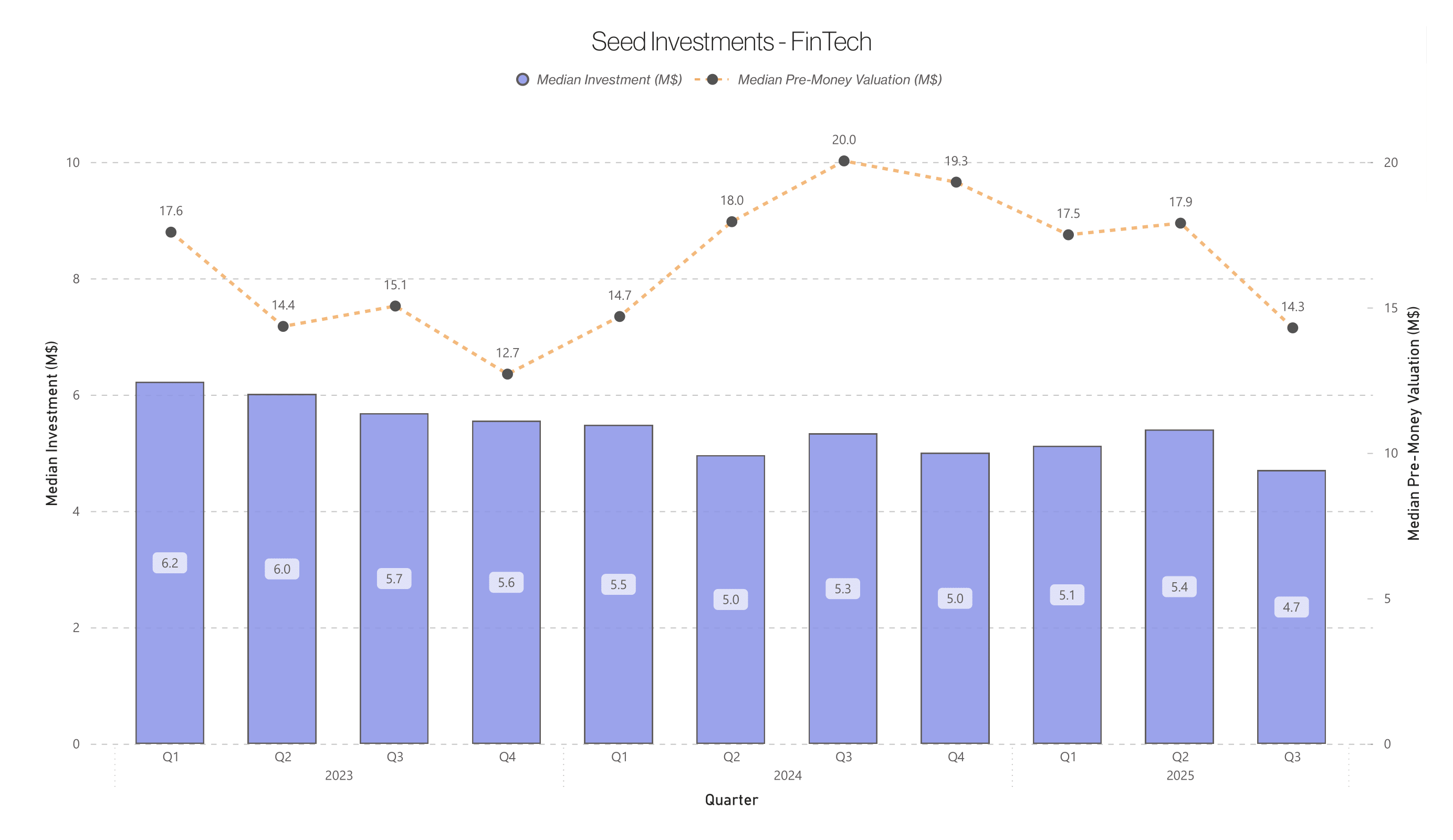

After a strong start to the year, FinTech seed activity slowed in Q3 2025 as valuations continued to stabilize. The median round stood at $4.7M, with a $14.3M median pre-money. Rounds remain within the post-2023 range, while valuations have settled from last year’s highs, signaling a more disciplined market.

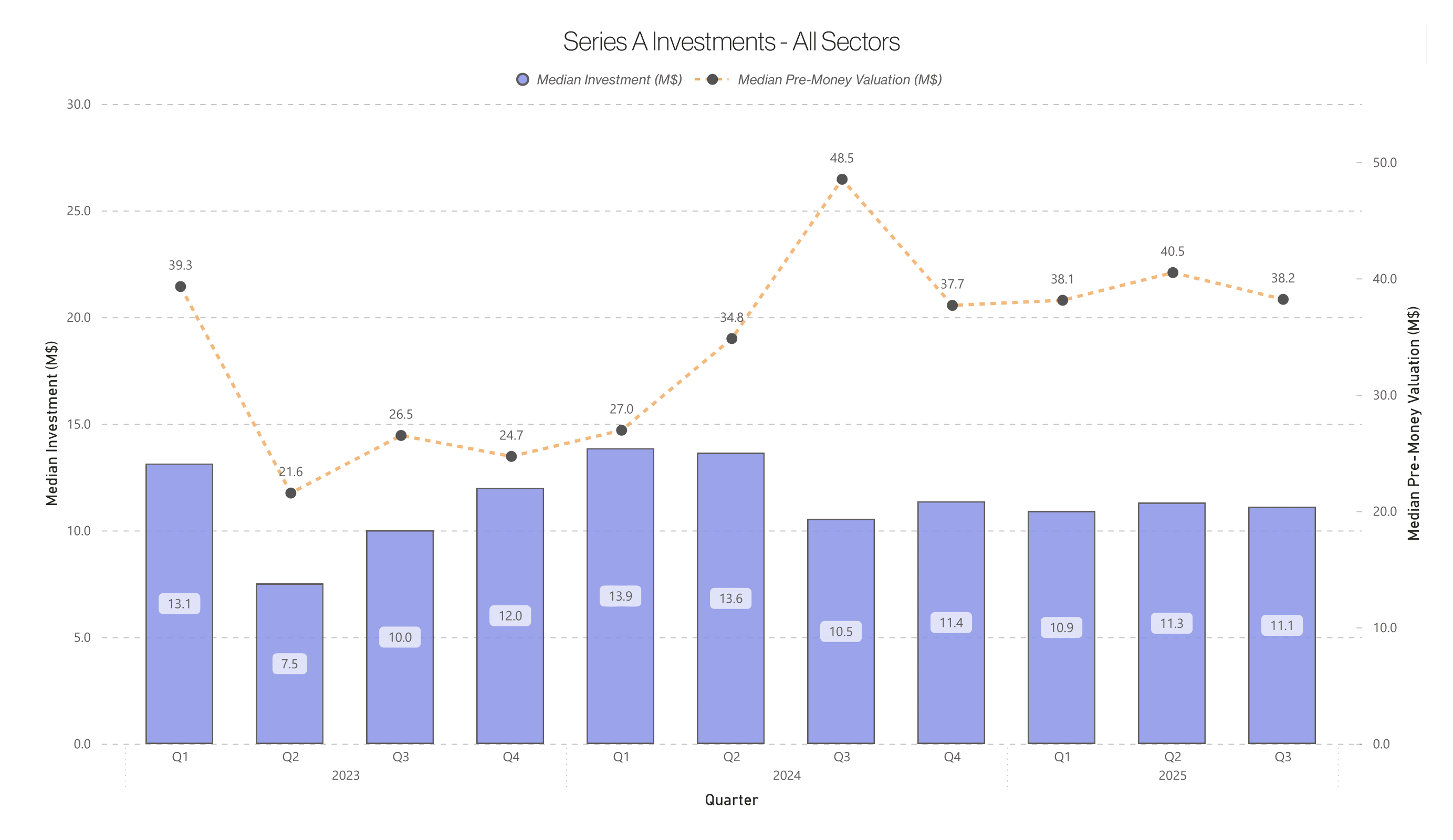

Series A activity across all sectors remained stable in Q3 2025. The median round reached $11.1M, with a $38.2M median pre-money valuation - slightly below Q2 2025. Compared to Q3 2024, rounds are a bit higher while valuations have leveled, signaling a market that remains active yet increasingly disciplined.

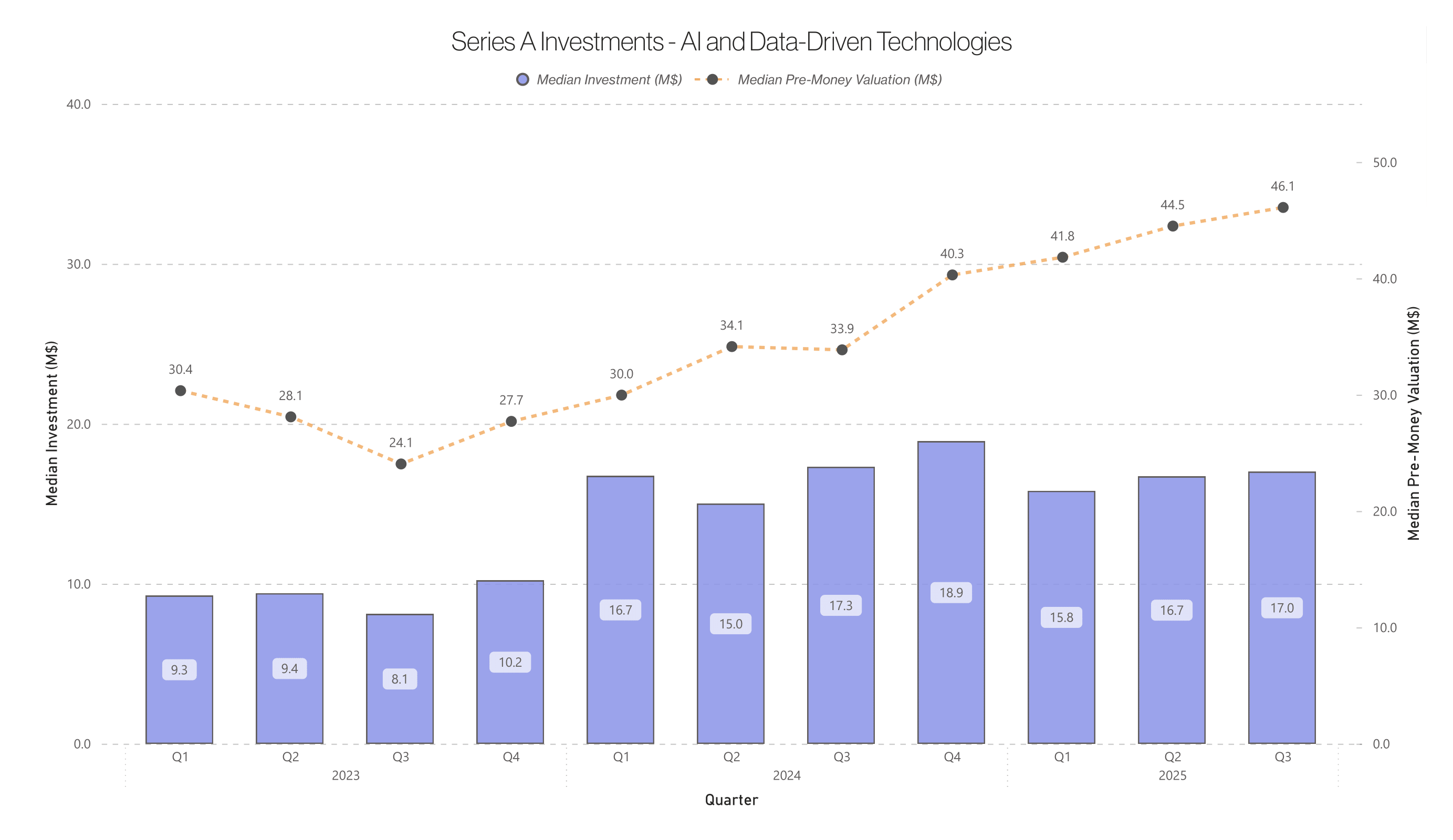

Series A funding in AI & Data-Driven Technologies continued to rise in Q3 2025. The median round reached $17.0M, with a $46.1M median pre- money. While round sizes remain steady year over year, valuations are on the rise, underscoring growing investor confidence in AI-driven innovation.

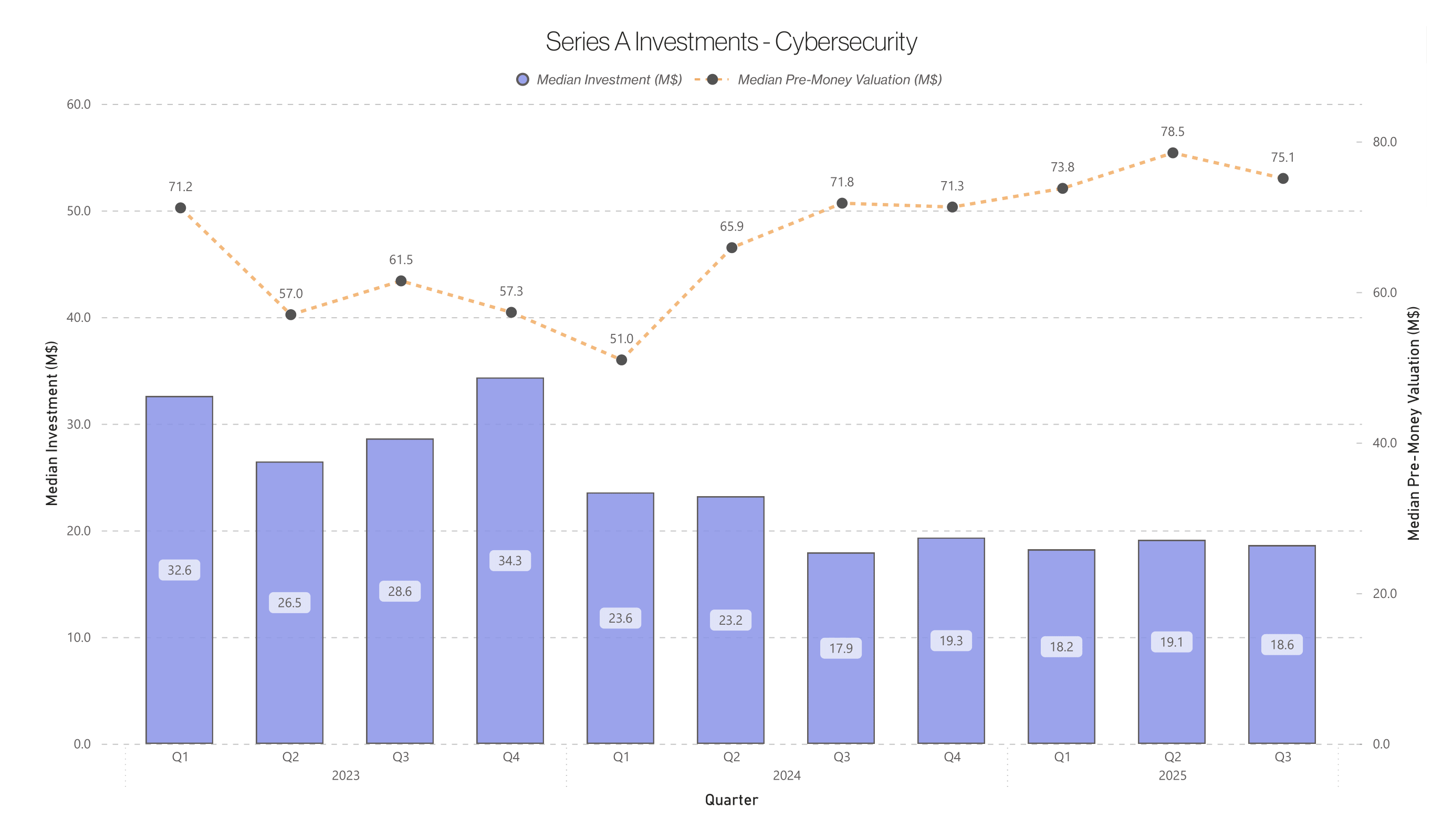

Series A funding in Cybersecurity held steady in Q3 2025. The median round reached $18.6M, with a $75.1M median pre-money valuation, signaling a resilient sector maintaining strong investor demand.

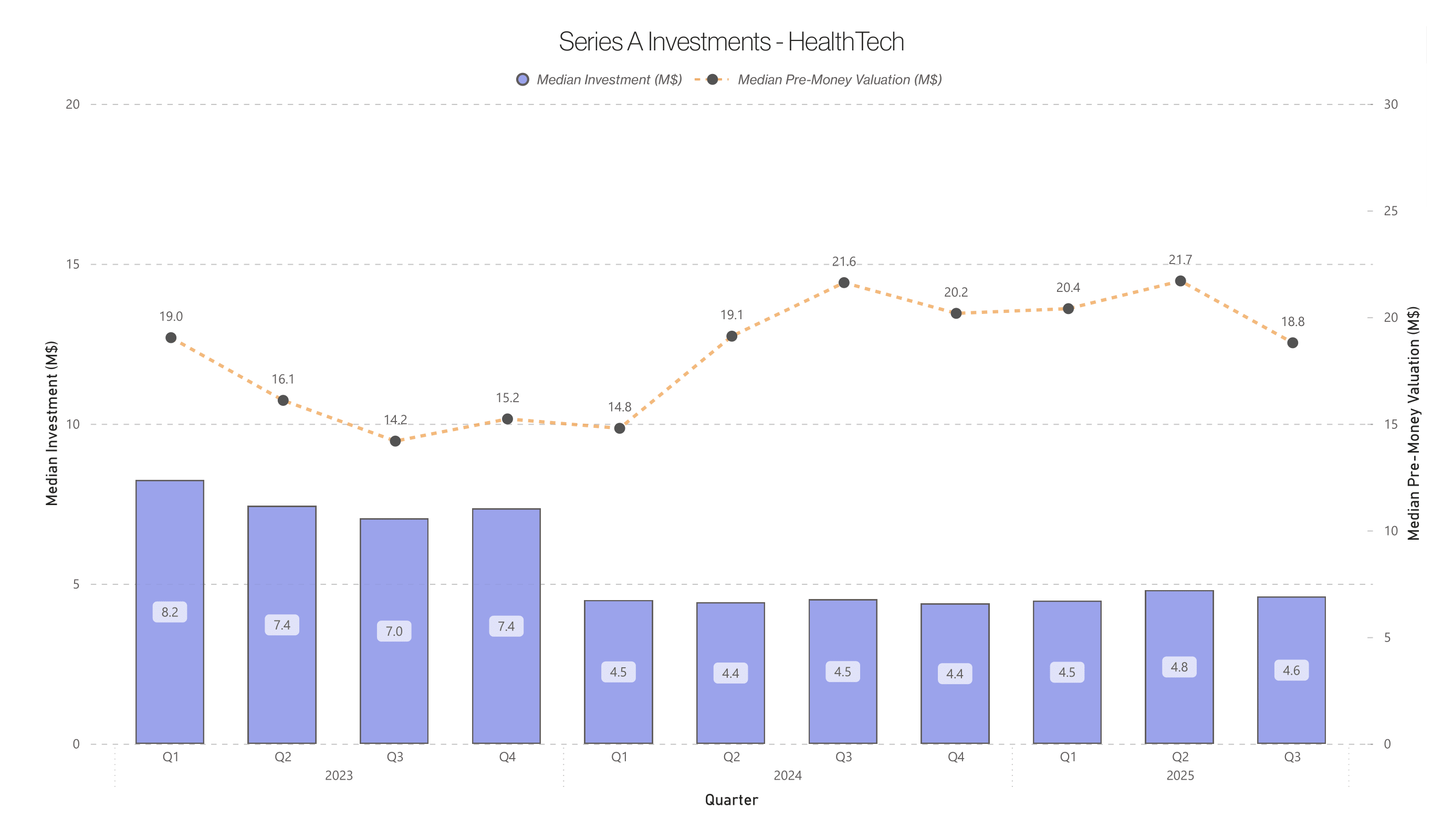

Series A funding in HealthTech softened in Q3 2025, with a $4.6M median round and a $18.8M median pre-money valuation. Round sizes held steady year over year, while valuations edged lower, signaling a more cautious but steady investment environment.

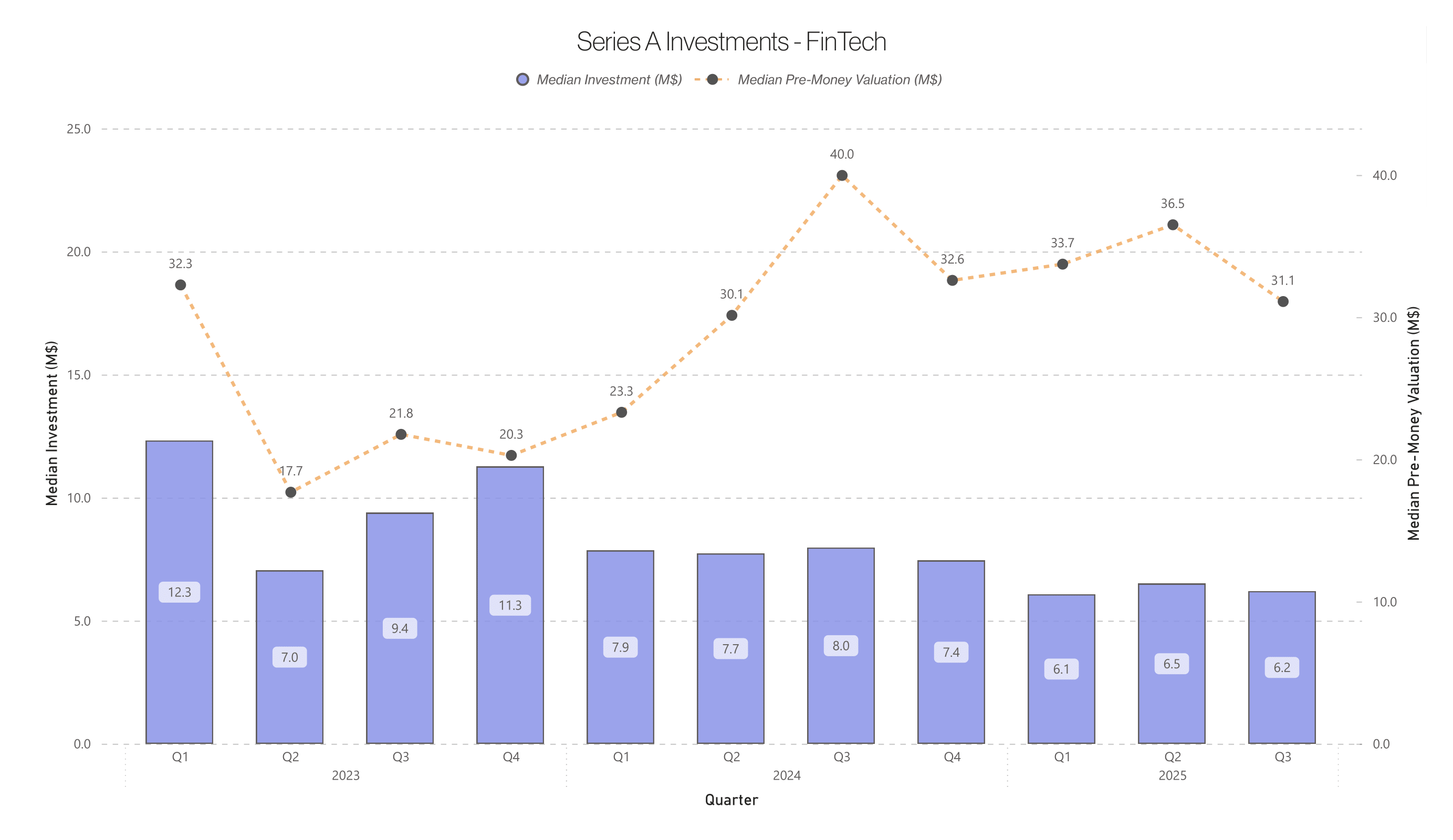

Series A funding in FinTech slowed slightly this quarter, with both round sizes and valuations easing after a strong 2024. The sector remains active and within its post-2023 range, though investors appear more measured as the market finds its footing.

Rounds held steady this quarter while valuations moved in different directions across sectors. AI/Data led with growth in bot h rounds and valuations.

Cybersecurity stayed strong, FinTech cooled, and HealthTech slowed at both Seed and Series A.

Momentum is clearly with AI/Data, while Cyber remains stable. FinTech and HealthTech are adjusting, mainly on valuations. Investors aren’t pulling back — they’re being more selective and focused on real traction.

The broad rebound has shifted into a more thoughtful market. AI/Data continues to earn a premium, while other sectors face tougher questions on value and proof.

The focus now is on clarity, performance, and strong stories that stand out.

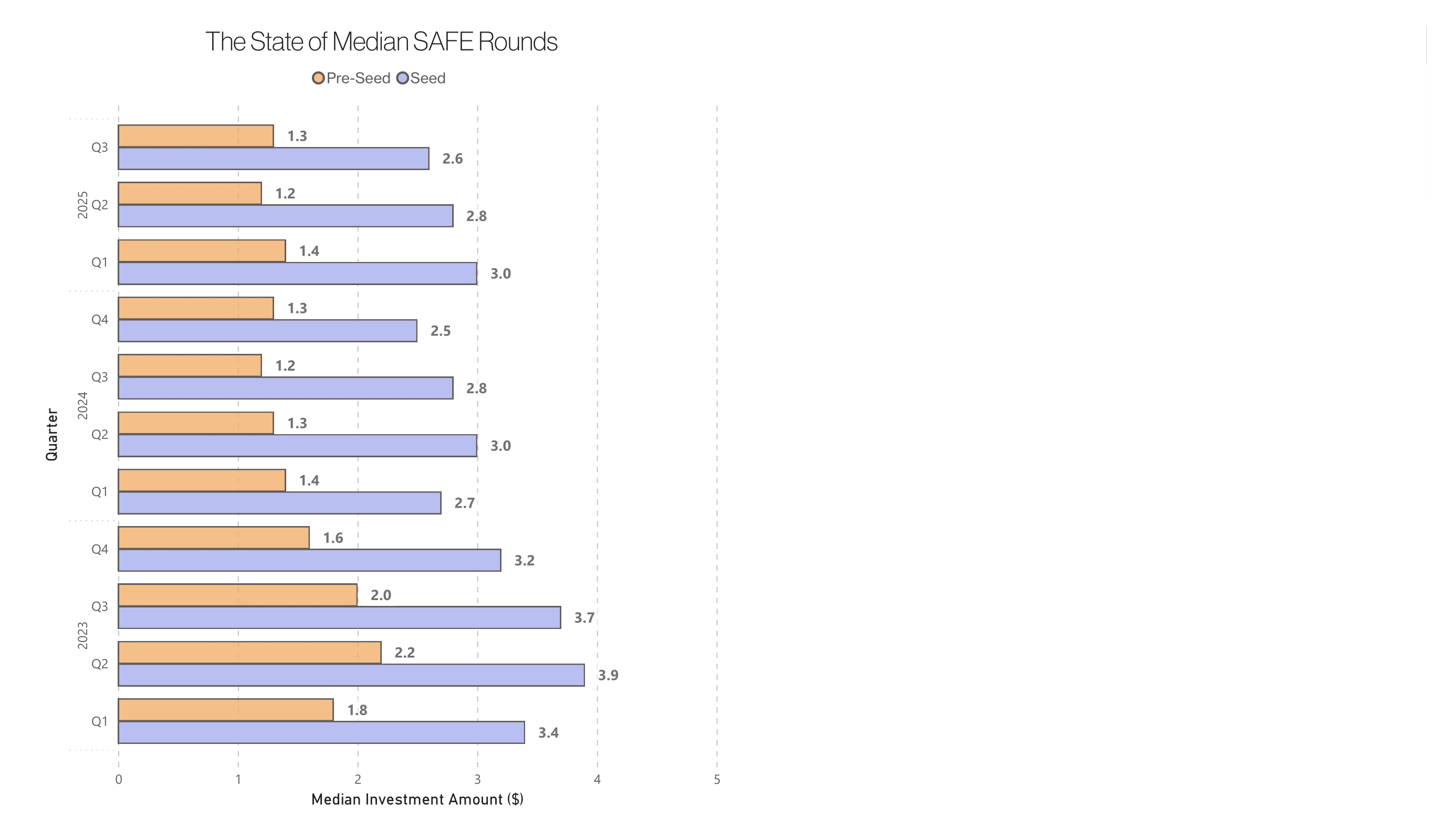

• The State of Median SAFE Rounds

This chart compares median SAFE round sizes at pre-seed and seed stages from early 2023 through Q3 2025. Round sizes have remained steady across both stages, with Q3 2025 medians at $1.3M for pre-seed and $2.6M for seed. Pre-seed rounds have held near $1.2–1.4M, and seed between $2.5–3.0M, maintaining a consistent 2× step-up as companies move from pre-seed to seed.

The pattern highlights stable early-stage dynamics despite broader market fluctuations.

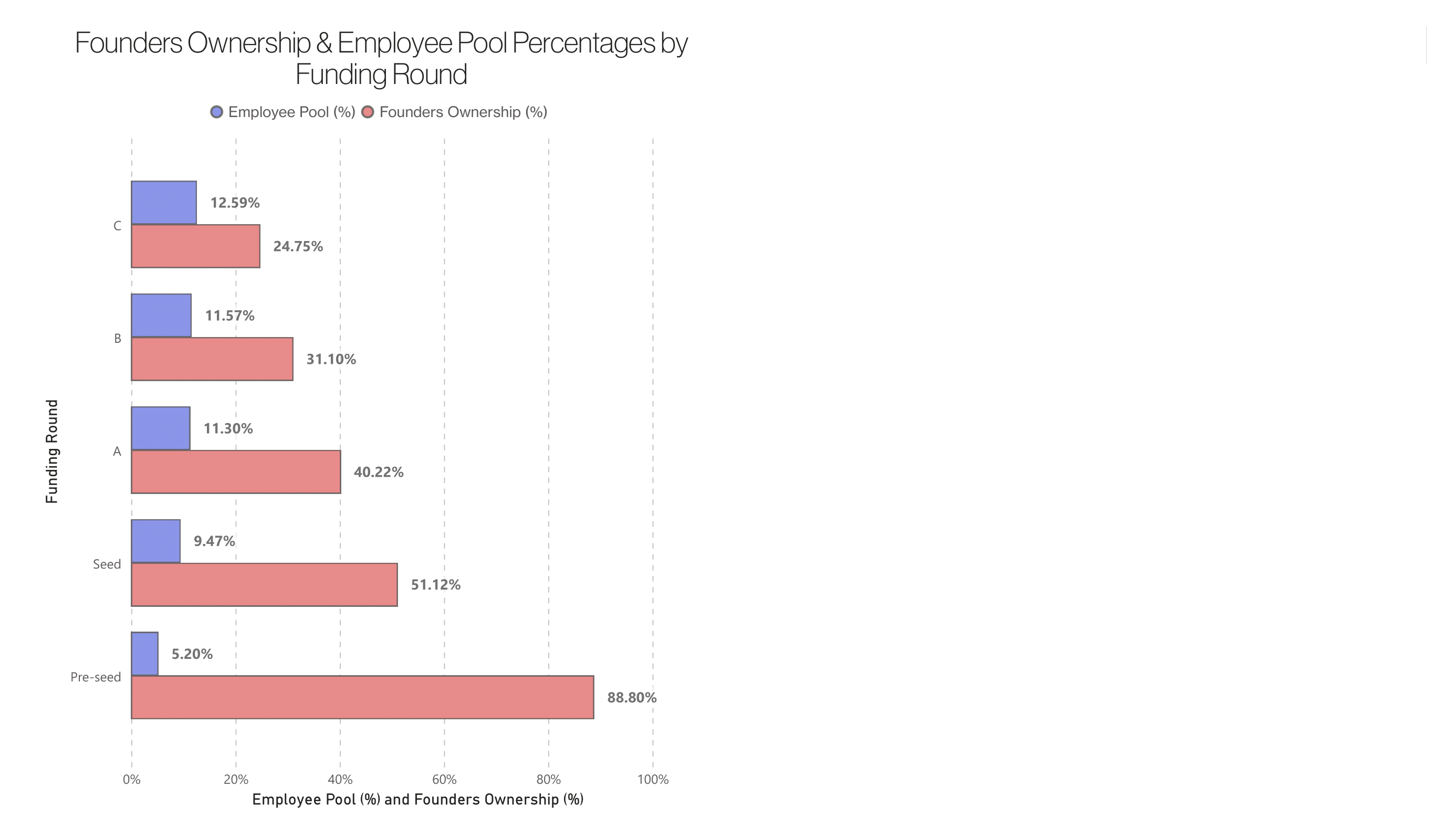

• Founders Ownership & Employee Pool Percentages by Funding Round

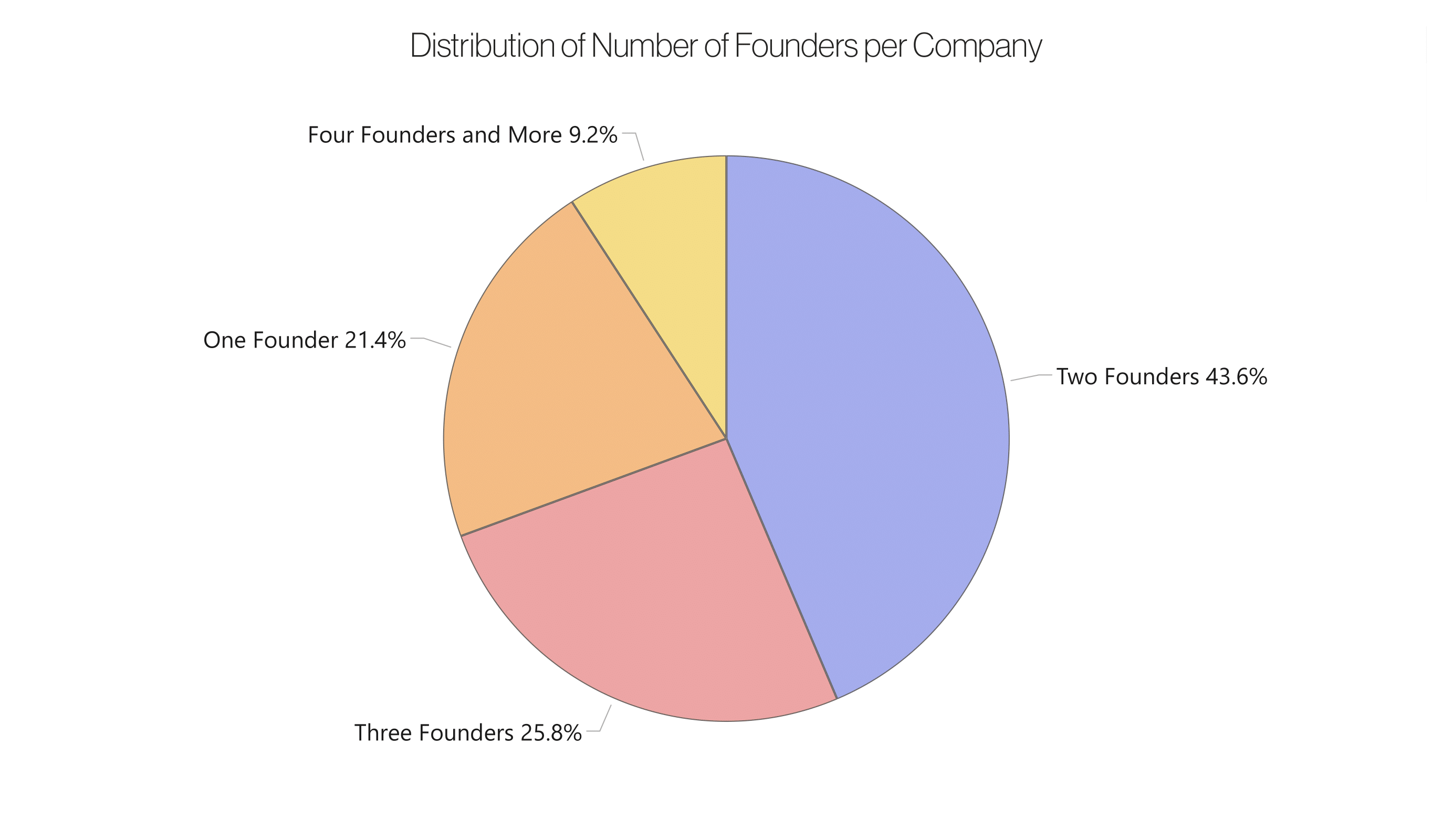

• Distribution of Number of Founders per Company

This chart shows the distribution of founders per company. Most startups are founded by two or three people, while solo founders make up a smaller but meaningful share and teams of four or more are uncommon. The data suggests that smaller, complementary teams strike the right balance, big enough to cover key areas like product, tech, and go-to-market yet small enough to stay aligned. This structure often leads to clear direction and healthier equity splits compared with larger teams or solo founders.

This chart compares founder ownership and employee option pools from pre-seed to Series C.

As companies raise more capital, founder ownership steadily decreases while employee pools grow. Each new round often brings a pool refresh and some founder dilution. Larger early pools can limit future increases, while smaller ones usually need expansion to support hiring.

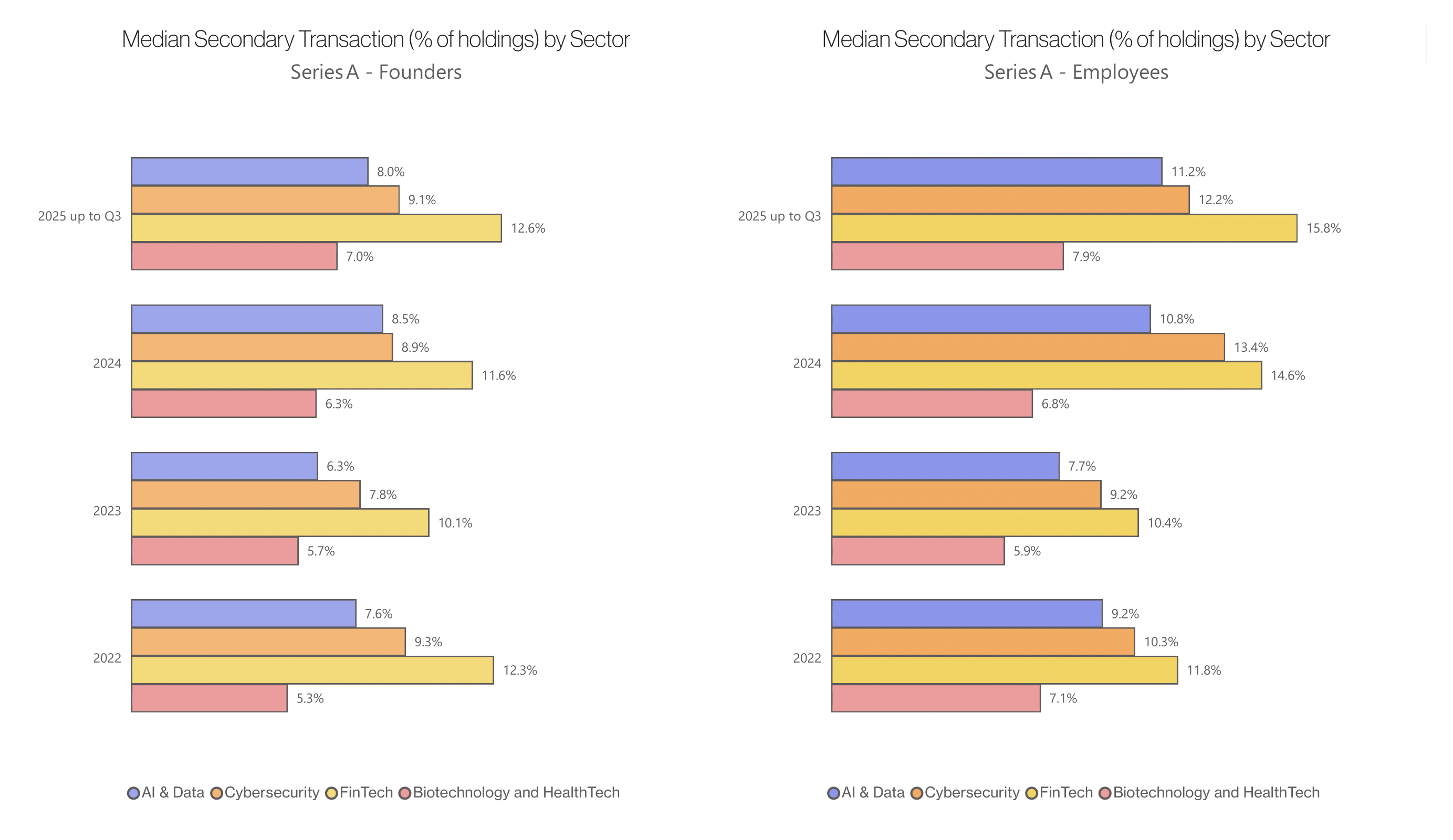

• Median Secondary Transactions By Sector – Series A

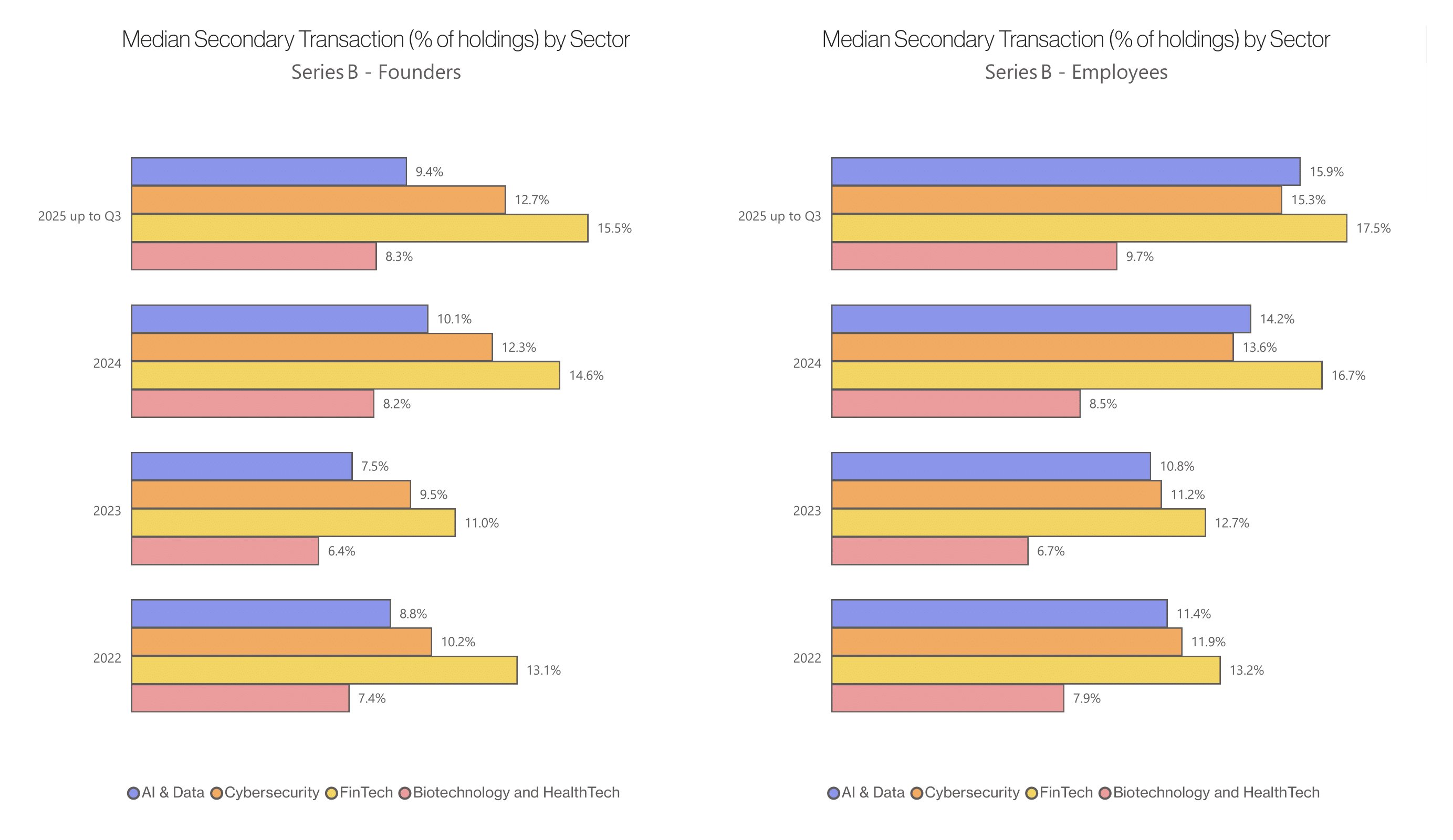

• Median Secondary Transactions By Sector – Series B

The slides on secondary activity compare median secondary transactions (as a percent of holdings) for founders and employees at Series A and Series B, across sectors from 2022 through Q3 2025. The analysis includes only material transactions, defined as sales above 2.5 percent of individual holdings.

Two clear trends stand out. Secondary events are larger at Series B than Series A, and employees consistently sell a higher share than founders

across all sectors. The sector ranking remains steady: FinTech leads in secondary activity, Cybersecurity and AI/Data follow, and Bio/Health stays

the most conservative.

Lower employee activity in earlier stages reflects vesting schedules and limited liquidity access. Most equity vests over four years with a one-year

cliff, meaning early employees often have fewer vested shares and limited sale windows. By Series B, more equity is vested, buyer demand

expands, and boards are more open to secondary programs, driving the clear increase from A to B.

Since 2023, secondary activity has grown steadily, especially among employees. At Series A, employee medians rose across sectors, with FinTech

reaching the mid-teens, while founder sales grew more modestly. At Series B, both groups saw increases, with FinTech maintaining the highest

levels and Bio/Health showing gradual but consistent growth.

• Revenue Multiples – By Sectors and Years

These figures reflect future revenue multiples, showing how valuations have evolved across sectors from H1 2022 to Q3 2025. AI and Data-Driven Technologies now lead as investors double down on AI adoption, while Cybersecurity remains strong with steady spending and rising awareness of digital threats.

HealthTech lost ground in 2023 but rebounded as AI workflows and clearer business models took shape.

FinTech, hit early by macro and regulatory pressures, continues to rebuild as fundamentals improve. Part of the shift may also result from changes in future revenue expectations, not only valuation levels, underscoring how market sentiment and forecast adjustments often move together.

• Exit Timing Delays

This chart shows how exit timelines have shifted in recent years, comparing companies that stayed on schedule with those that delayed by one year or more.

Delays peaked in 2023 and 2024, when many teams chose to wait out a tight liquidity market and focus on extending runway.

In 2024 and 2025, we see a partial reset. More companies are moving forward as planned, showing stronger confidence, while one-year delays remain common.

These often reflect hesitation rather than a clear decision. Multi-year deferrals, on the other hand, usually signal a deliberate choice to postpone until reaching stronger scale or profitability.

Overall, the market is reopening and founders appear more decisive about their path to liquidity.

About altshare

altshare is a leading, fast-growing Equity Management & Compensation Plans Administration solutions provider. We love challenges. We are obsessed with our clients. We are on a mission to redefine the way founders do equity. All our products & services are supported through the altshare Platform - the only equity management platform built for entrepreneurs.