This report is issued by and on behalf of altshare Ltd. ("altshare") for informational purposes only and shall not be construed as legal, financial, or tax advice.

The information contained in this report is based on data provided to and/or prepared by altshare for its clients. The report is based on an aggregated and anonymized data from altshare's clients.

While this report may address potential legal, financial, and/or tax matters, it does not constitute professional advice in these areas. The opinions or conclusions expressed herein are not to be attributed to altshare. We strongly recommend that you seek the counsel of qualified advisors before taking any actions based on the information provided in this report.

For the avoidance of doubt, altshare shall not assume any liability for, nor be held responsible for any damages, losses, claims, or expenses, whether direct, indirect, incidental, consequential, special, or punitive, arising from the use or reliance on the information contained in this report. altshare shall not be liable for any actions taken or not taken based on the information contained herein.

altshare does not warrant the accuracy, completeness, or reliability of the data presented and assumes no responsibility for any errors or omissions. The information provided in this report is subject to change without notice.

This report is provided "as is" and altshare disclaims any responsibility for the outcomes of decisions made by the recipient or any third party in reliance on its contents.

• Seed Rounds by Sector

• Series A Rounds by Sector

• The State of Median SAFE Rounds

Between early 2023 and mid-2024, seed-stage investments across all sectors experienced a significant decline, marked by a notable decrease in both median investment amounts and pre-money valuations.

This period was characterized by higher investor selectivity and stricter capital allocation due to challenging market conditions. However, current data indicates the market is entering a stabilization phase, with projections suggesting investment levels and valuations will remain steady or show modest recovery through 2025.

This trend signifies a fundamental recalibration of market expectations and highlights the inherent resilience of early-stage investment activity.

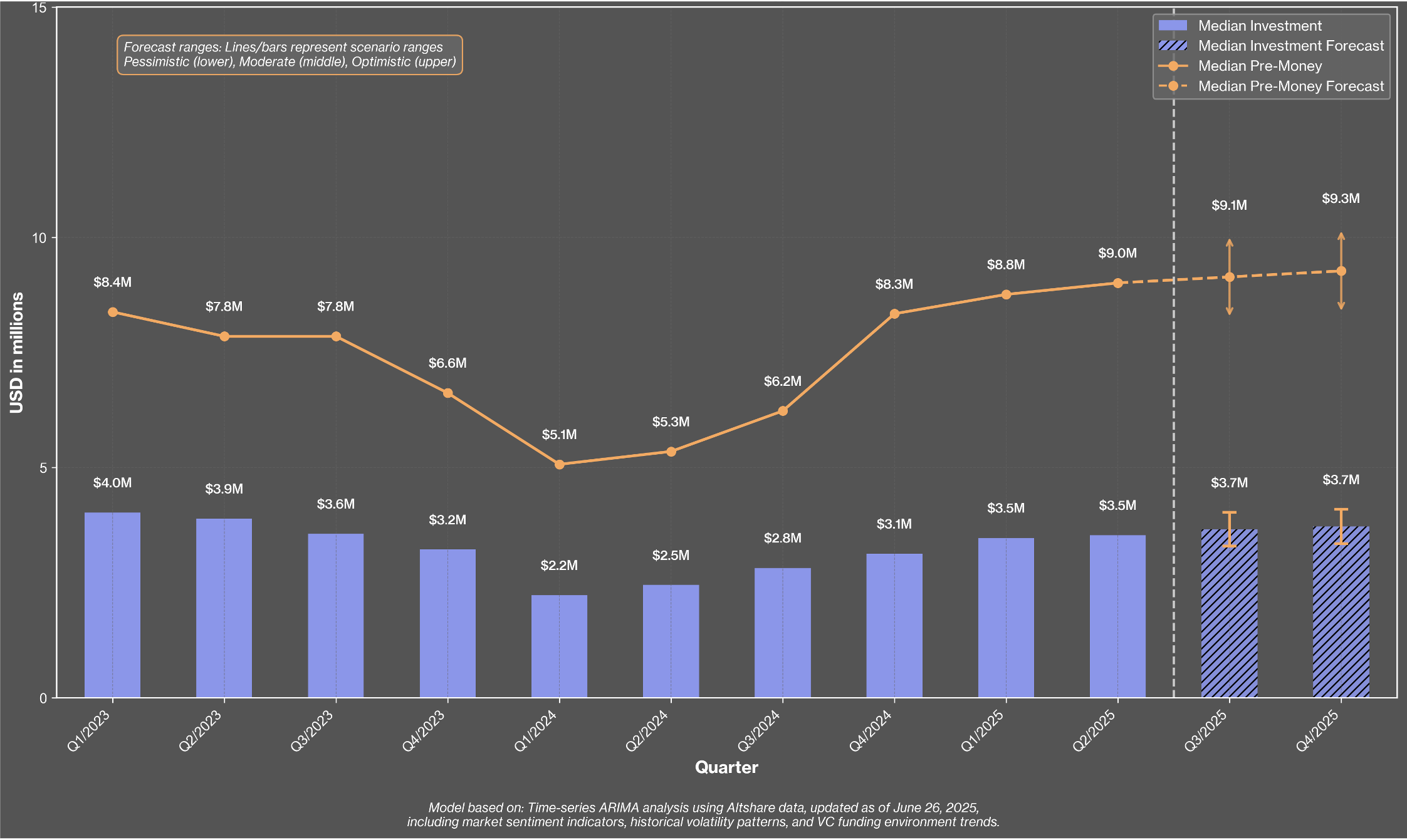

The AI and Data-Driven Technologies sector demonstrated resilience during the recent market downturn.

While valuations saw a decline in 2023, this drop was much less severe compared to the overall market. By late 2023, signs of recovery began to emerge.

Looking ahead, strong indicators suggest that robust investment activity and high pre-money valuations will continue through 2025.

This performance underscores ongoing investor confidence in AI-driven solutions, as they are willing to pay premium prices for quality opportunities within this sector.

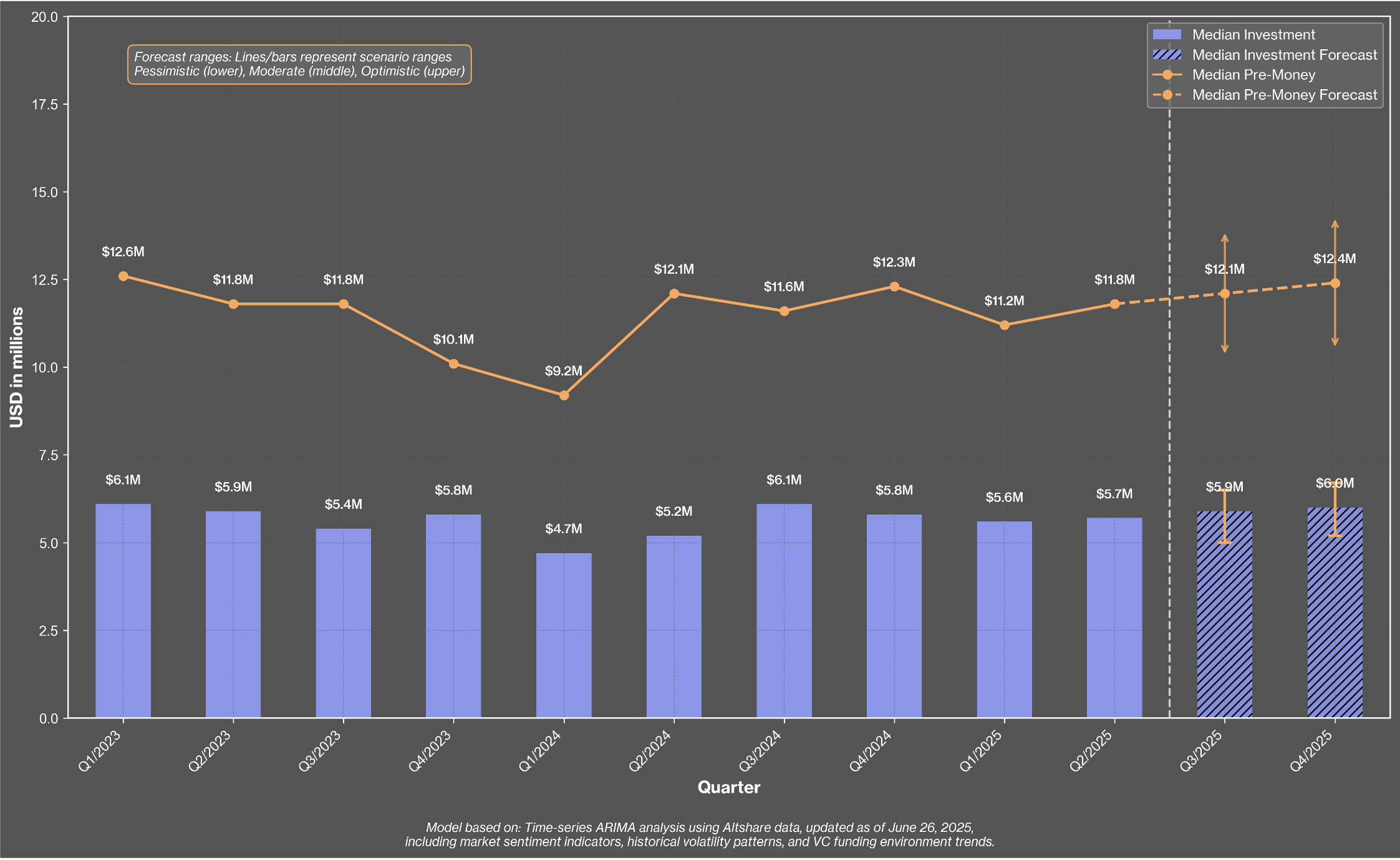

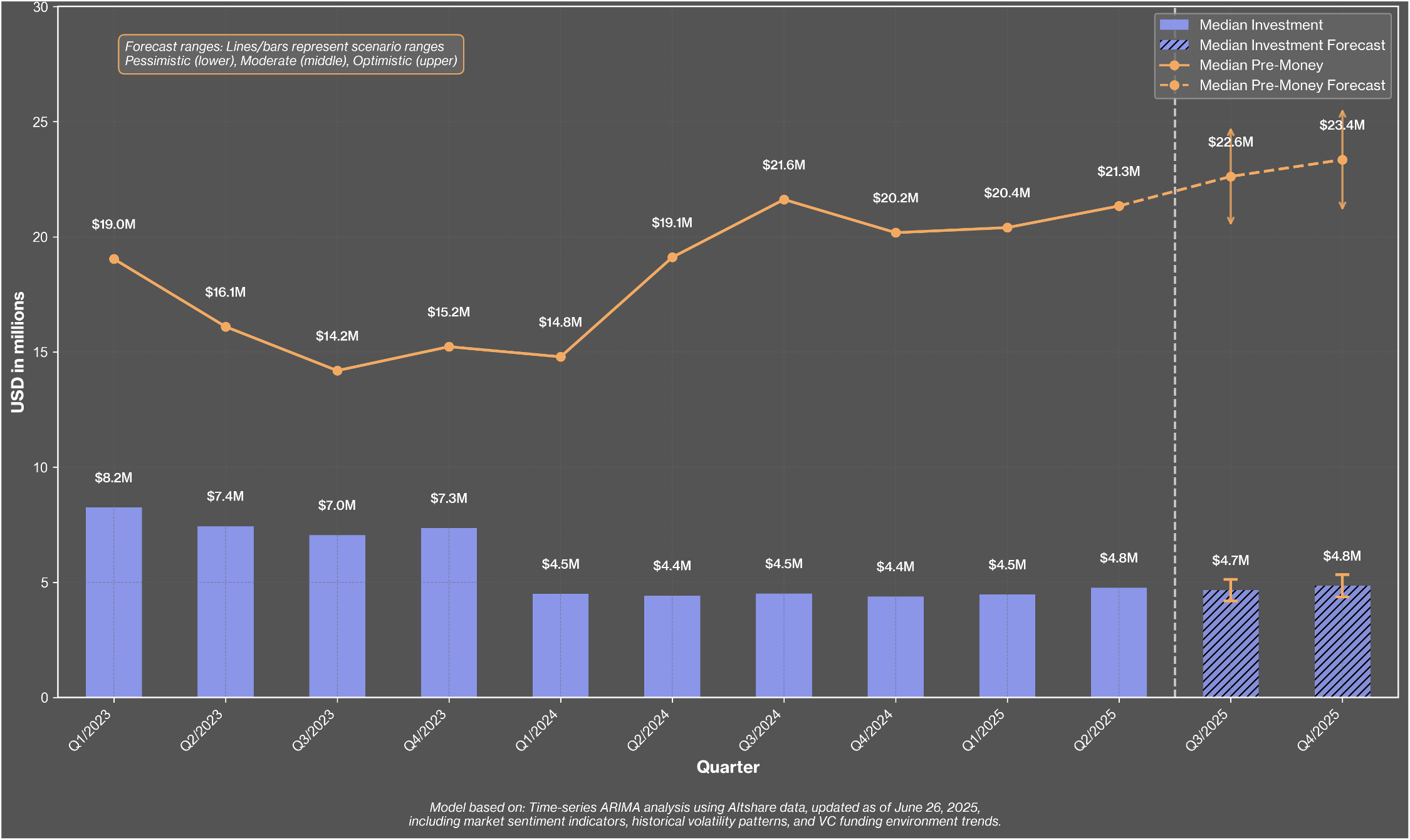

Biotechnology and HealthTech companies at the Seed stage saw a sharp decline in valuations from 2023 to 2024.

This drop resulted from decreased investor interest in early-stage biotech, especially amid rising interest rates and stricter capital allocation.

The biggest declines occurred in ventures without clear clinical or regulatory progress.

However, by late 2024, the sector began to recover, thanks to renewed interest in AI-assisted diagnostics, preventative health, and more public sector investment in healthcare resilience.

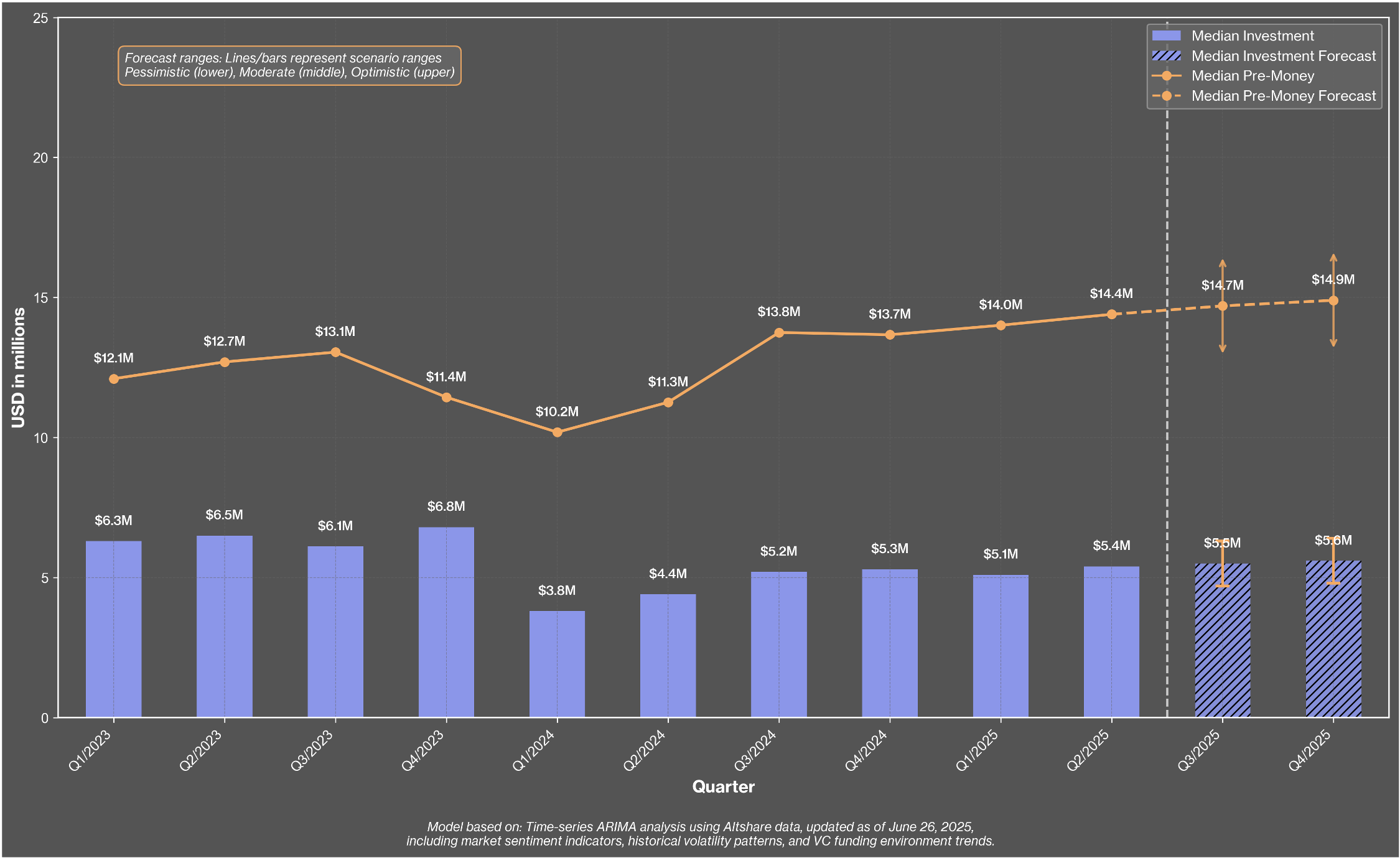

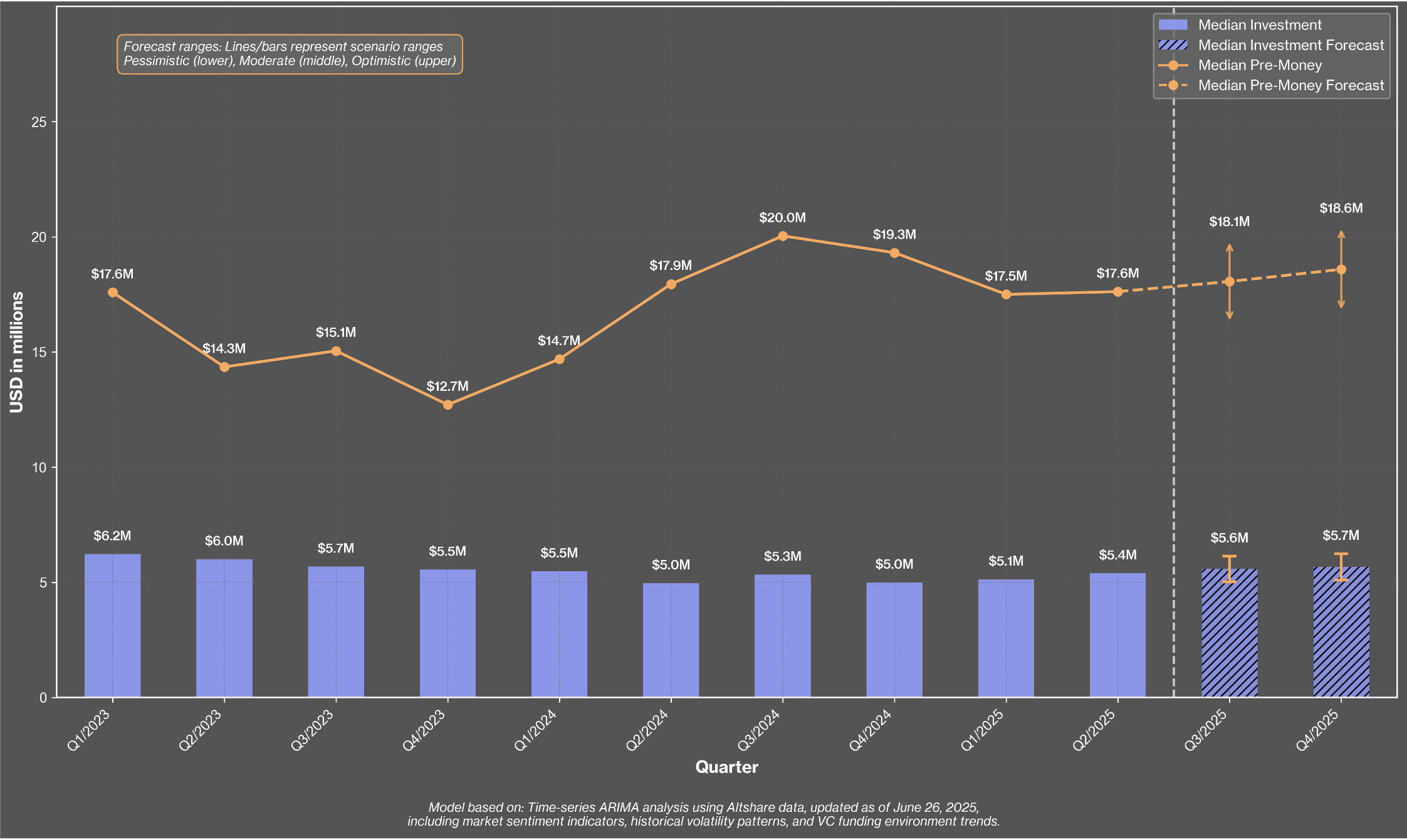

Cyber security showed remarkable resilience during the Seed stage throughout this period.

Pre-money valuations held steady and the sizes of funding rounds were consistently larger than in many other sectors.

The ongoing global threat landscape, marked by high-profile cyberattacks an increased national security concerns, maintained strong interest from investors.

Startups led by teams with security backgrounds or connections to military or intelligence units attracted significant capital, often receiving valuations typically seen in later-stage companies from other sectors.

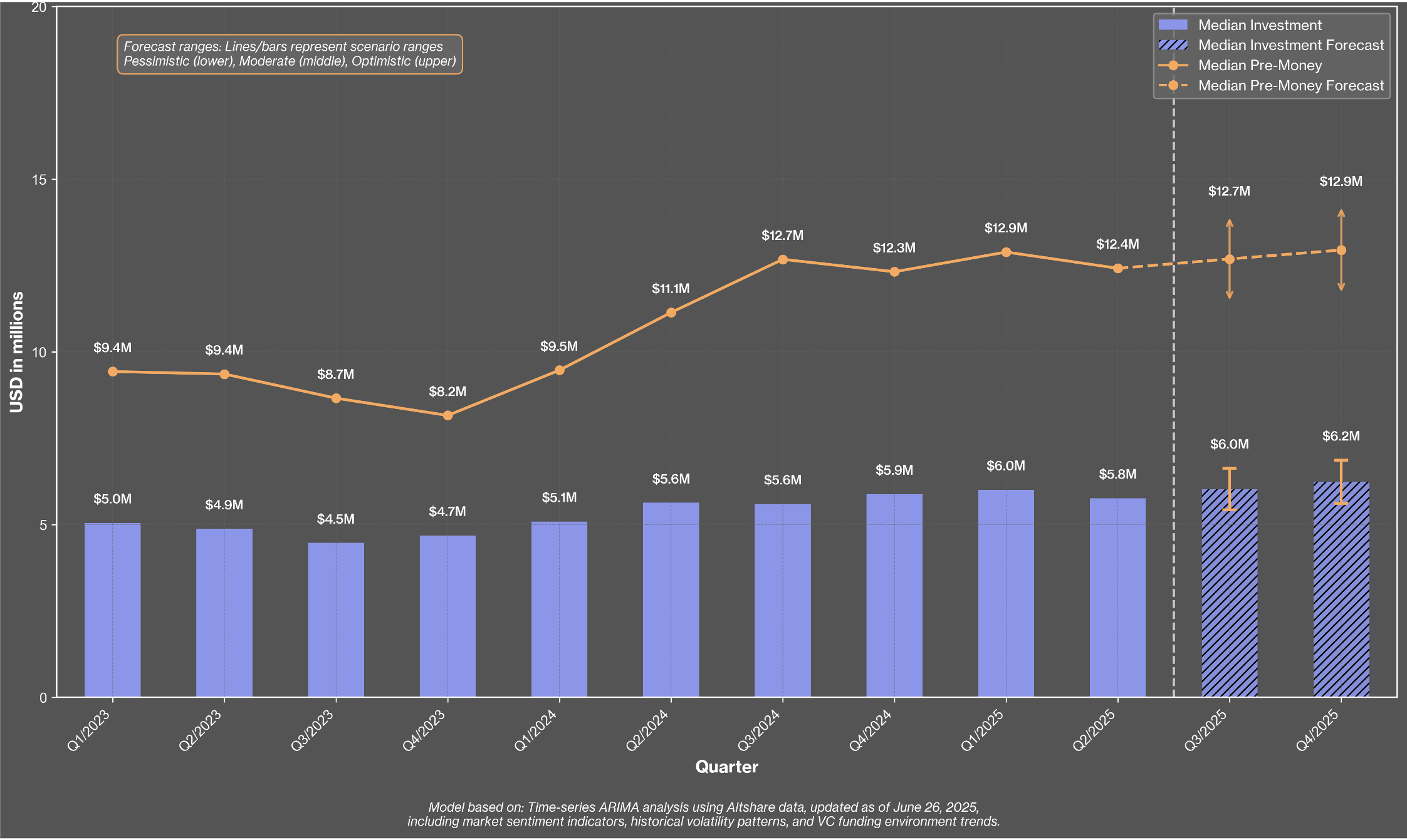

In 2023, FinTech startups at the Seed stage faced a significant drop in valuations as investor confidence waned due to regulatory changes and fatigue from oversubscribed consumer models.

By 2024, market sentiment started to improve, with capital returning to the sector more cautiously and focusing on sustainable unit economics.

Investors leaned toward B2B solutions, especially in infrastructure, compliance, and embedded finance. The rebound in valuations and consistency in funding rounds reflect a more disciplined funding environment, favoring teams with clear monetization strategies and strong product-market fit.

The Seed investment landscape over the past 18 months shows a market reset followed by sector-specific recoveries influenced by investor confidence and risk tolerance.

FinTech leads in pre-money valuations, consistently above $17M, peaking at $20M, though check sizes are moderate, indicating cautious investment. Cybersecurity displays steady growth, with rising valuations and investment amounts, signaling healthy confidence.

AI and Data Driven Tech startups have seen the fastest valuation recovery, rebounding to record highs by late 2025, but median investment sizes remain subdued.

Biotech and HealthTech have made a strong V-shaped recovery, surpassing pre-downturn valuations, yet check sizes are still below 2023 averages.

Overall, the Seed market is stabilizing, with diverging strategies: some investors seek growth and long-term disruption, while others are refocusing on sustainable early-stage economics.

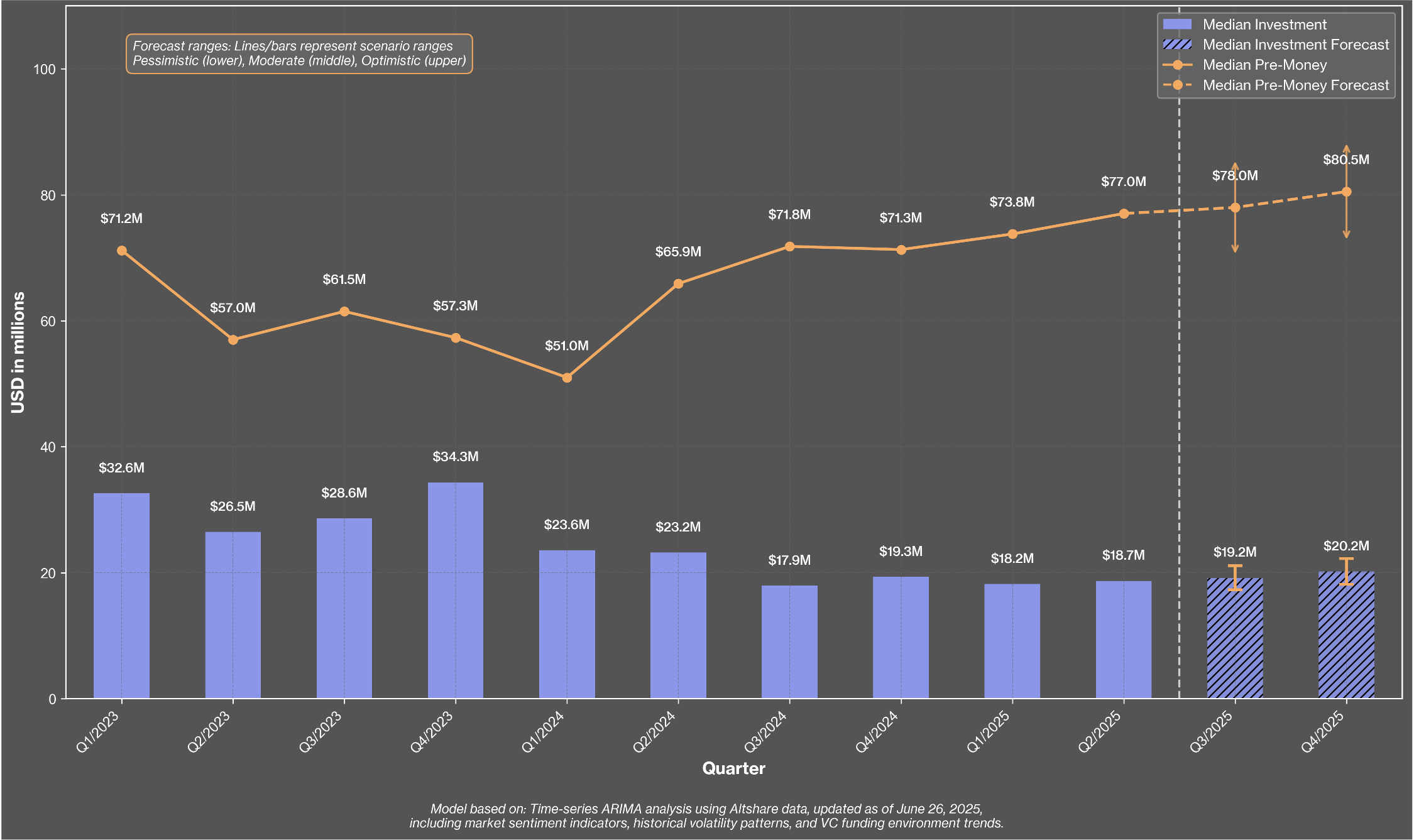

This chart illustrates the median investment amounts and pre-money valuations for Series A funding across various sectors.

Unlike the seed stage, Series A investments have shown more resilience during the market downturn, experiencing only a slight decline in both investment size and valuations. This was followed by a steady recovery.

Since late 2023, there's been a consistent upward trend, indicating that institutional investors are regaining confidence and that competition for high-quality Series A deals is still strong.

Looking ahead, forecasts suggest continued stabilization and even modest gains, creating an environment where only the most compelling companies are able to attract significant capital.

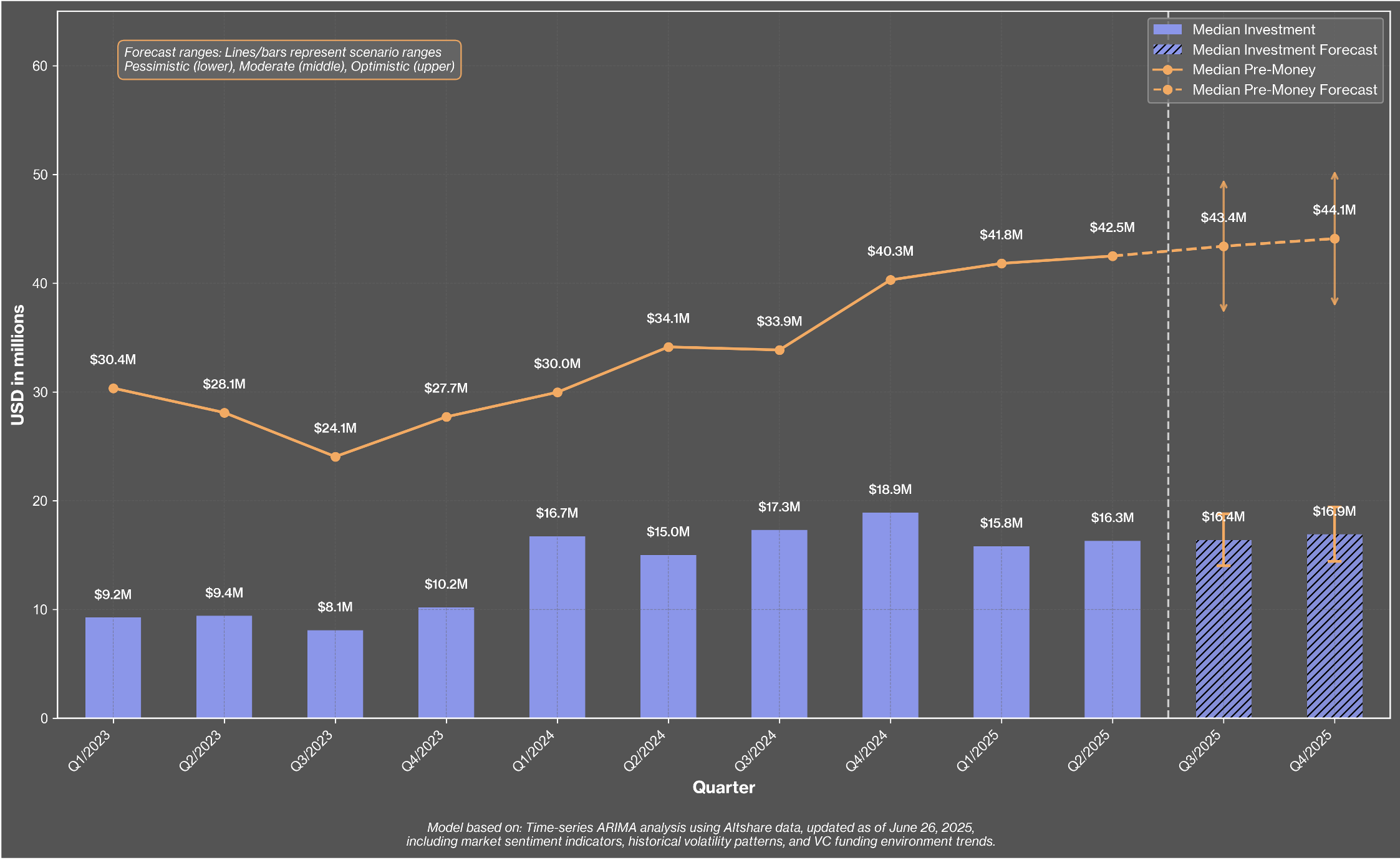

The AI and Data-Driven Technologies sector at the Series A stage is bouncing back quickly and showing strong valuations.

After a brief decline, both median investment amounts and pre-money valuations are rising steadily, outpacing the broader market. This quick recovery highlights strong confidence from institutional investors.

Moving forward, forecasts indicate that AI will remain a key focus for investment, with high valuations and increased competition for leading companies expected throughout 2025.

In Series A funding rounds, Biotechnology and HealthTech faced a milder decline compared to earlier stages. While valuations fell gradually through 2023 and early 2024, they began to recover in 2025.

This rebound is likely due to investor interest in companies demonstrating early clinical success or forming key B2B partnerships.

Although funding is still cautious compared to previous cycles, the rising valuations reflect increasing confidence in the sector’s long-term potential and technological viability.

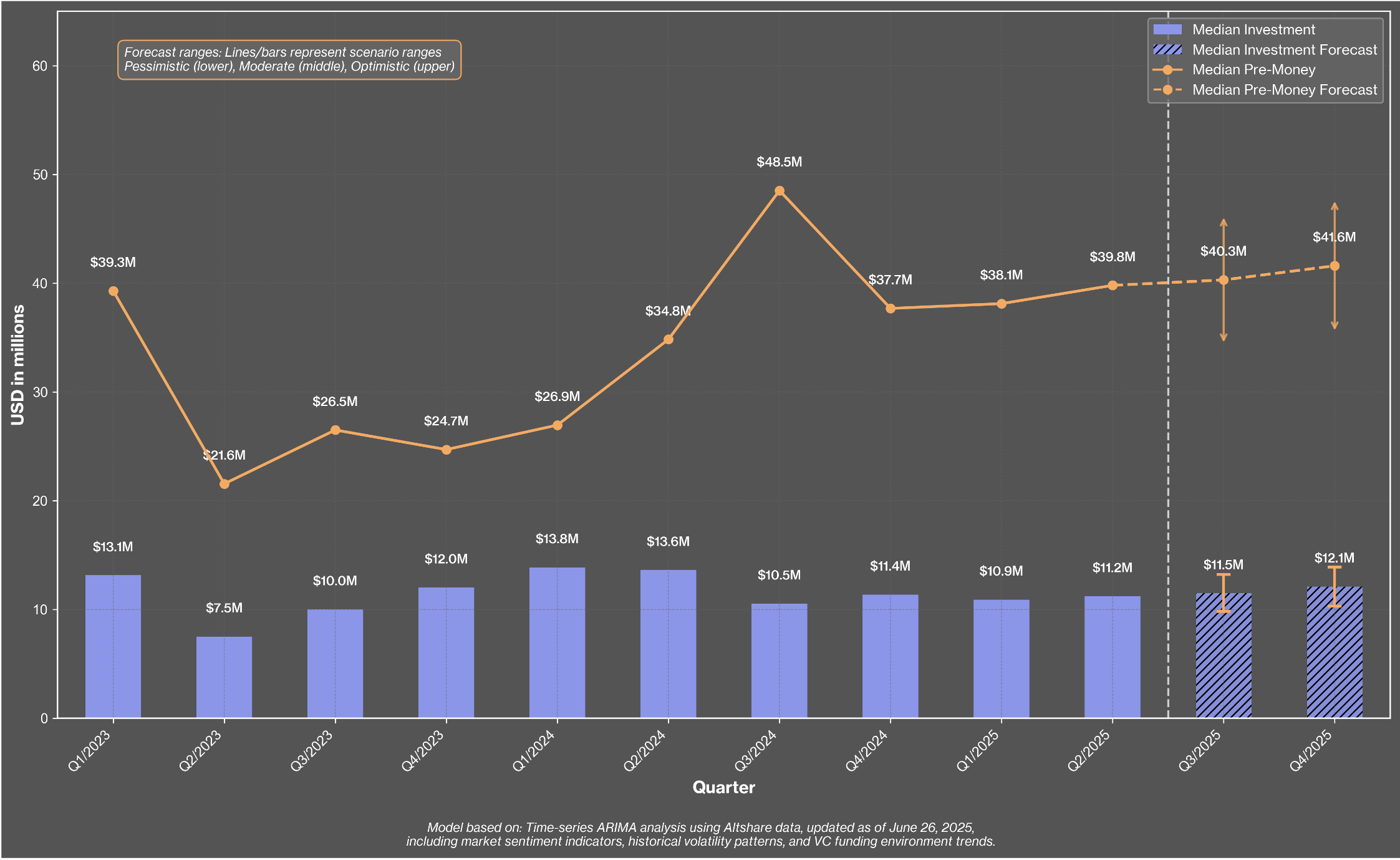

As we move into 2024 and 2025, the Series A stage in Cybersecurity is drawing strong investor interest, reflected in rising valuations and sufficient capital.

Key drivers include increased cloud adoption, vulnerabilities in software supply chains, and regulatory pressures.

As businesses expand their attack surfaces, particularly in identity, operational technology, and third-party integrations, Series A companies offering unique and scalable solutions are gaining investor confidence. Many are designed with mergers and acquisitions in mind, attracting strategic investors early in their growth.

In the Series A stage, FinTech showed signs of recovery, reflecting a growing interest in infrastructure-focused financial technologies. Valuations rose from mid-2024, while growth remained steady and capital allocation careful.

Investors favored companies with regulatory-compliant APIs, vertical SaaS integrations, and strong financial back-end systems. Unlike past funding cycles, today’s FinTech sector values sustainable growth and operational efficiency, focusing on serving underserved markets instead of aggressive expansion.

The Series A landscape from 2023 to 2025 shows a clear shift from early-stage caution to a more confident approach in growth-stage investments. While 2023 was marked by volatility, investor behavior in 2024 and beyond reveals varied trends across sectors regarding pricing and capital allocation.

Cybersecurity stands out as the leader, with median pre-money valuations soaring to $80.5M by late 2025 and round sizes surpassing $20M, the highest of all sectors. This reflects strong confidence in recurring revenue models, robust B2B adoption, and the sector’s resilience. Close behind, AI and Data-Driven Technologies are experiencing the fastest and most consistent growth, with valuations jumping from $24.1M to $44.1M in less than two years, and median check sizes stabilizing above $16M.

In contrast, FinTech has seen a sharp recovery from its 2023 lows, nearing $37M by Q4 2025. However, investor participation remains limited, with round sizes around $7.5M, indicating a disconnect between market excitement and actual capital investment. Biotech and HealthTech sectors show a more cautious recovery, with valuations rebounding to roughly $23M but round sizes rarely exceeding $5M.

Overall, the Series A market is thriving, but investment strategies are becoming more selective by sector. Investors are eager to back companies with clear scalability and resilience while applying stricter criteria around capital intensity and timing for returns.

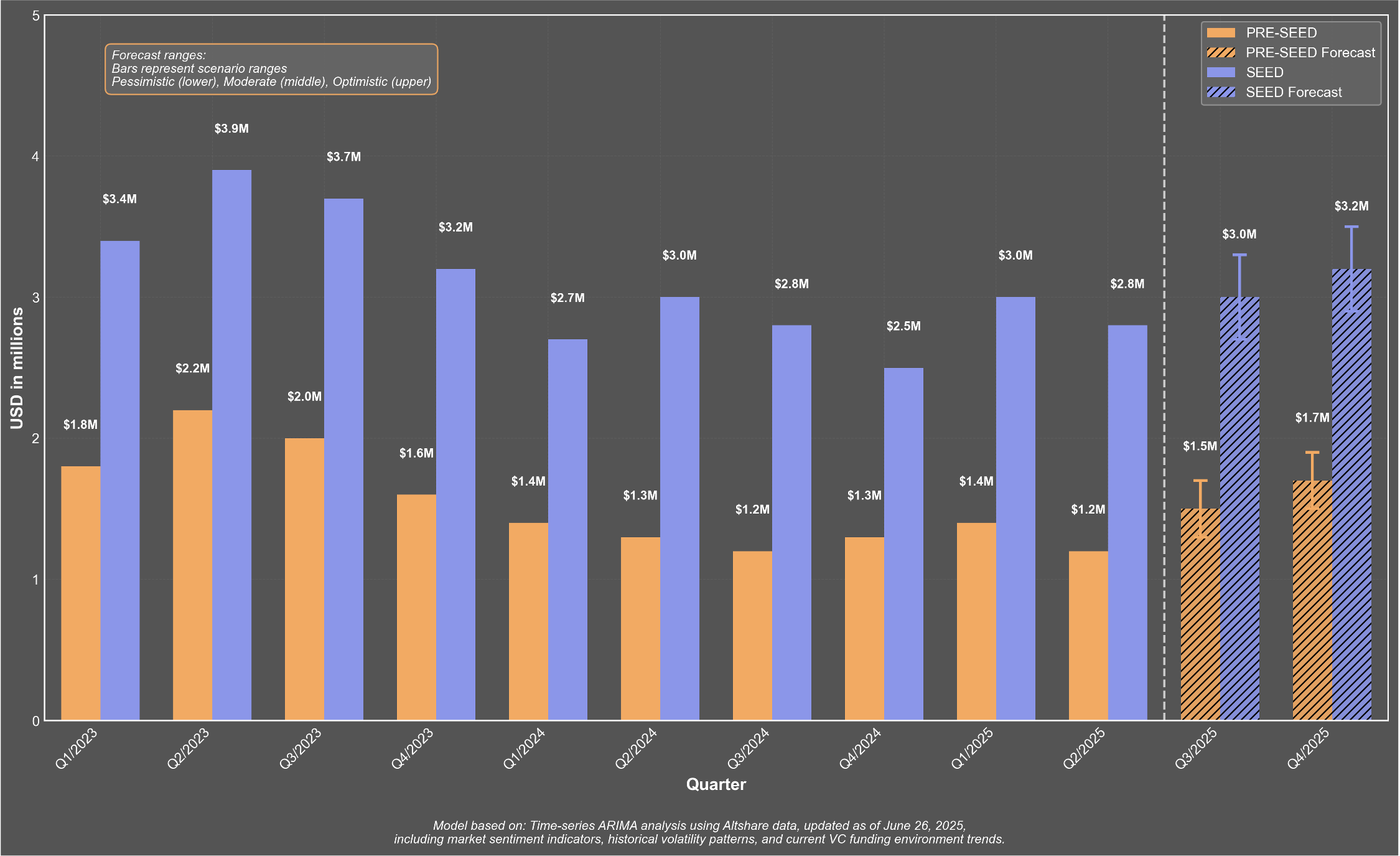

This chart showcases the evolution of Pre-Seed and Seed SAFE round sizes, reflecting a clear shift in early-stage funding behavior. During the 2021–2022 cycle, many founders raised sizable rounds on vision alone. Since then, SAFE rounds increasingly demand real signals - milestone progress, product traction, and capital discipline.

Round sizes declined through 2023 but have since stabilized. The forecast for late 2025 shows modest growth, hinting at cautious investor optimism while maintaining stricter standards.

Overall, the data reflects a more selective environment. Founders who demonstrate early execution are gaining traction, while narrative-led rounds are fading from the market.

• Volume Growth of Ordinary Shares

• Median Percentage of Ordinary Shares

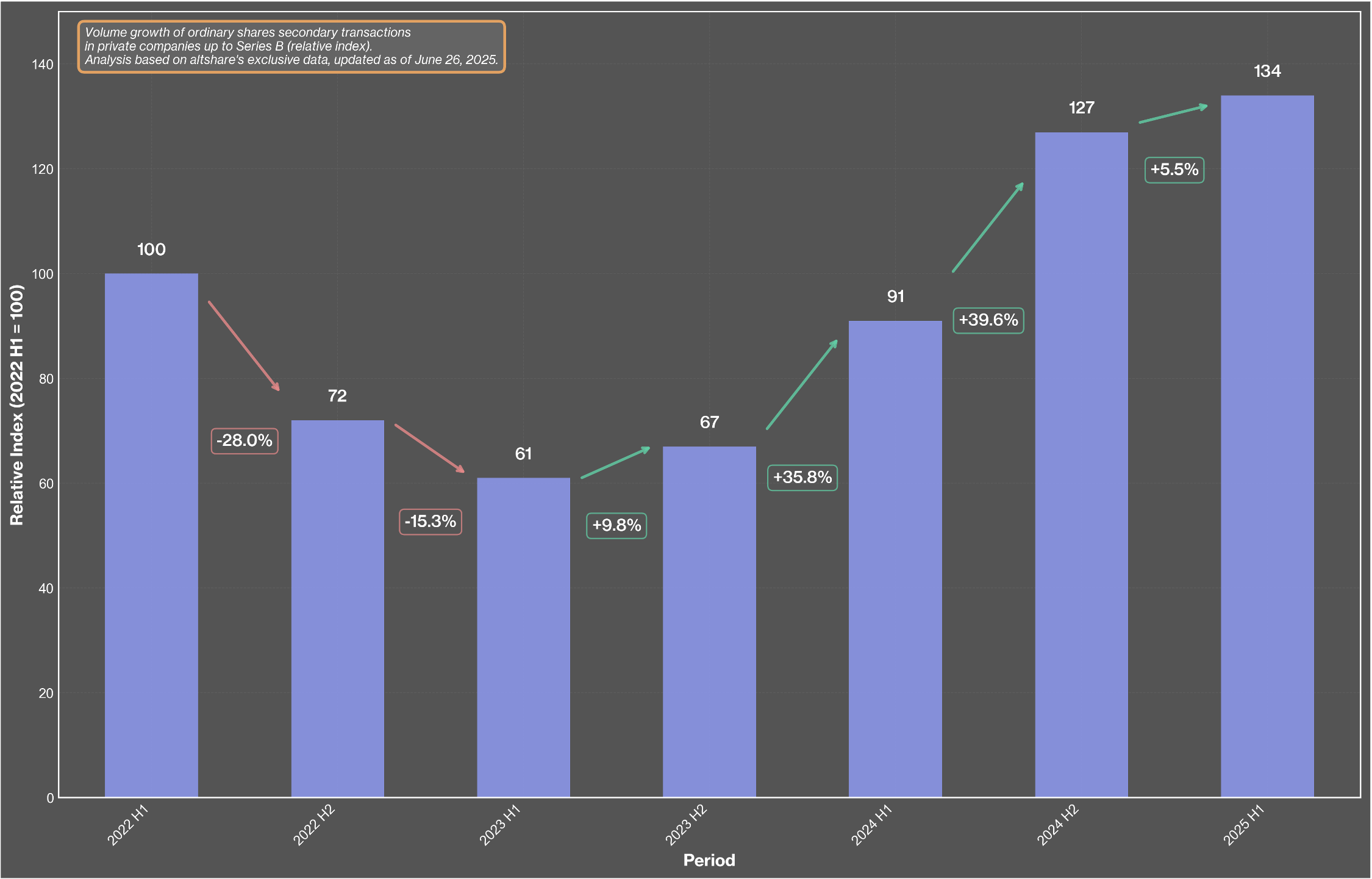

This chart shows the volume trend of secondary transactions in ordinary shares for private companies up to Series B, using a relative index (H1 2022 = 100). There was a sharp decline in activity from H1 2022 to H1 2023, likely due to economic uncertainty, funding constraints, or reduced interest in secondary deals.

However, from H2 2023 onward, the market steadily recovers, peaking in H2 2024, with transaction volumes nearly doubling from the 2023 lows.

This growth suggests a new balance between sellers and buyers, maturation of the secondary market, or more realistic valuations.

By H1 2025, the market stabilizes at a high activity level, likely due to increased internal liquidity and greater shareholder willingness for secondary transactions.

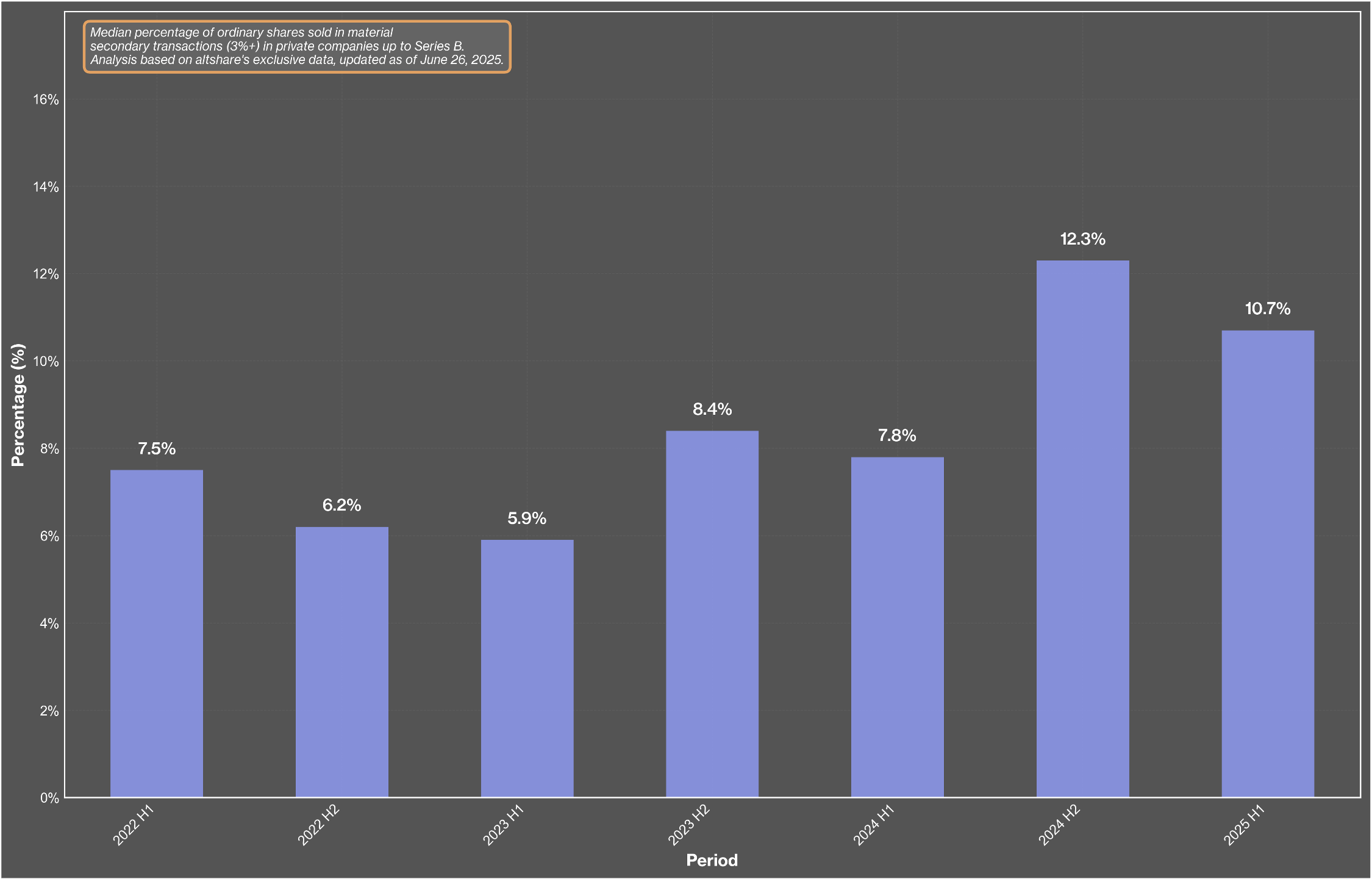

The chart displays the median percentage of ordinary shares sold in significant secondary transactions (over 3% of total ordinary shares) for private companies up to Series B, tracked every six months from 2022 to mid-2025.

After a gradual decline throughout 2022 and early 2023, secondary share sales began to rise again in H2 2023 and peaked in late 2024. This trend reflects growing liquidity needs among founders and early employees, alongside wider acceptance of secondary deals within venture financing. By H1 2025, activity stabilizes at higher levels, suggesting that secondaries have become a normalized tool.

Whether this shift signals a confident, maturing market or insider uncertainty remains an open question.

• Founders Ownership & Employee Pool Percentages by Funding Round

• Distribution of Number of Founders per Company

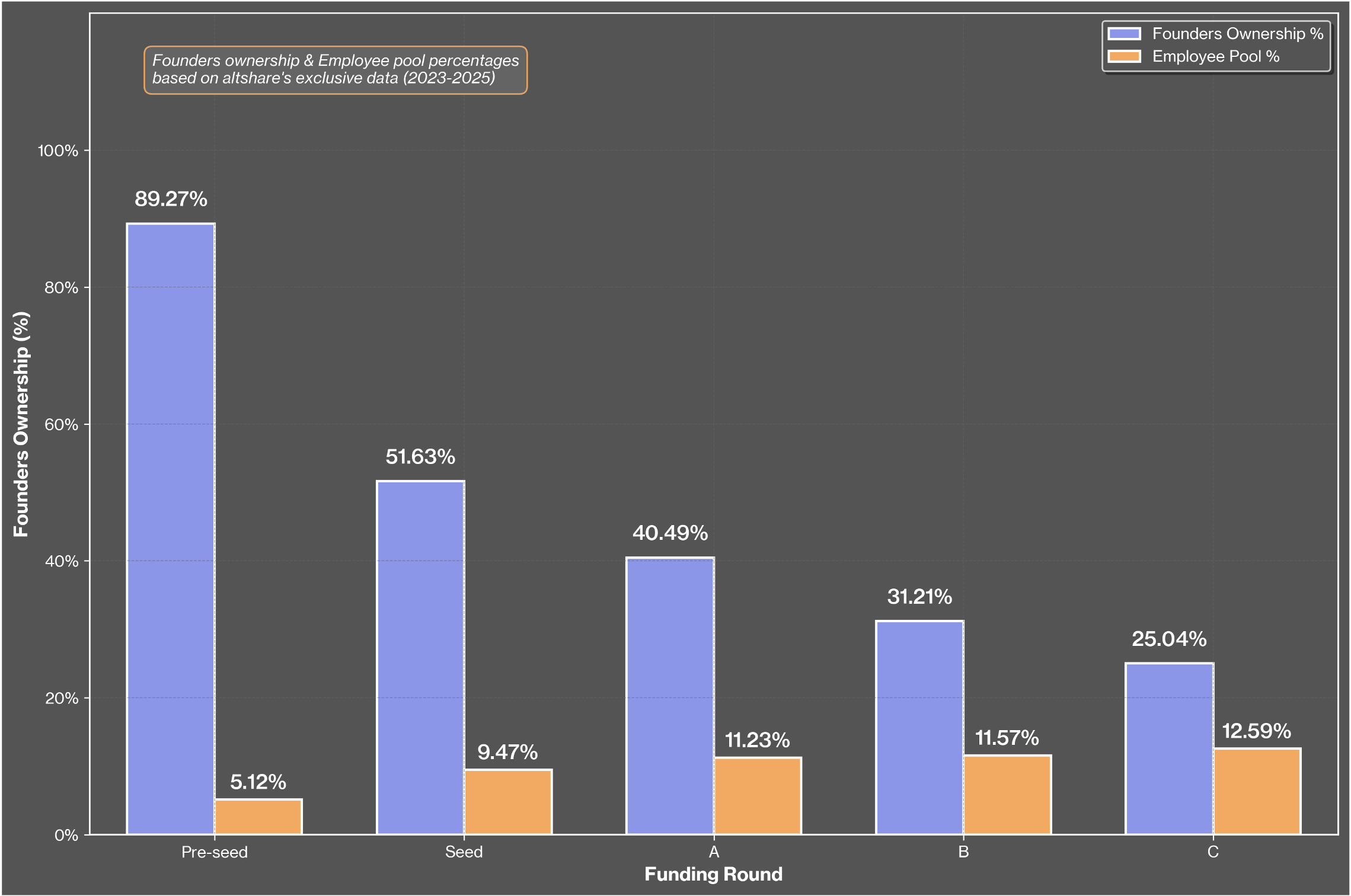

This bar chart shows the median founders' ownership percentages and employee equity pool sizes segmented by funding round, based on altshare's exclusive data from 2023 to 2025.

Founders start with nearly 90% ownership at the pre-seed stage, but this drops to around 25% by Series C.

Meanwhile, the employee pool grows early and then remains relatively stable at around 11–12% from Series A onward. This consistency suggests a standard market approach to employee incentives, with companies maintaining a steady equity pool size even as they scale, balancing dilution with retention across stages.

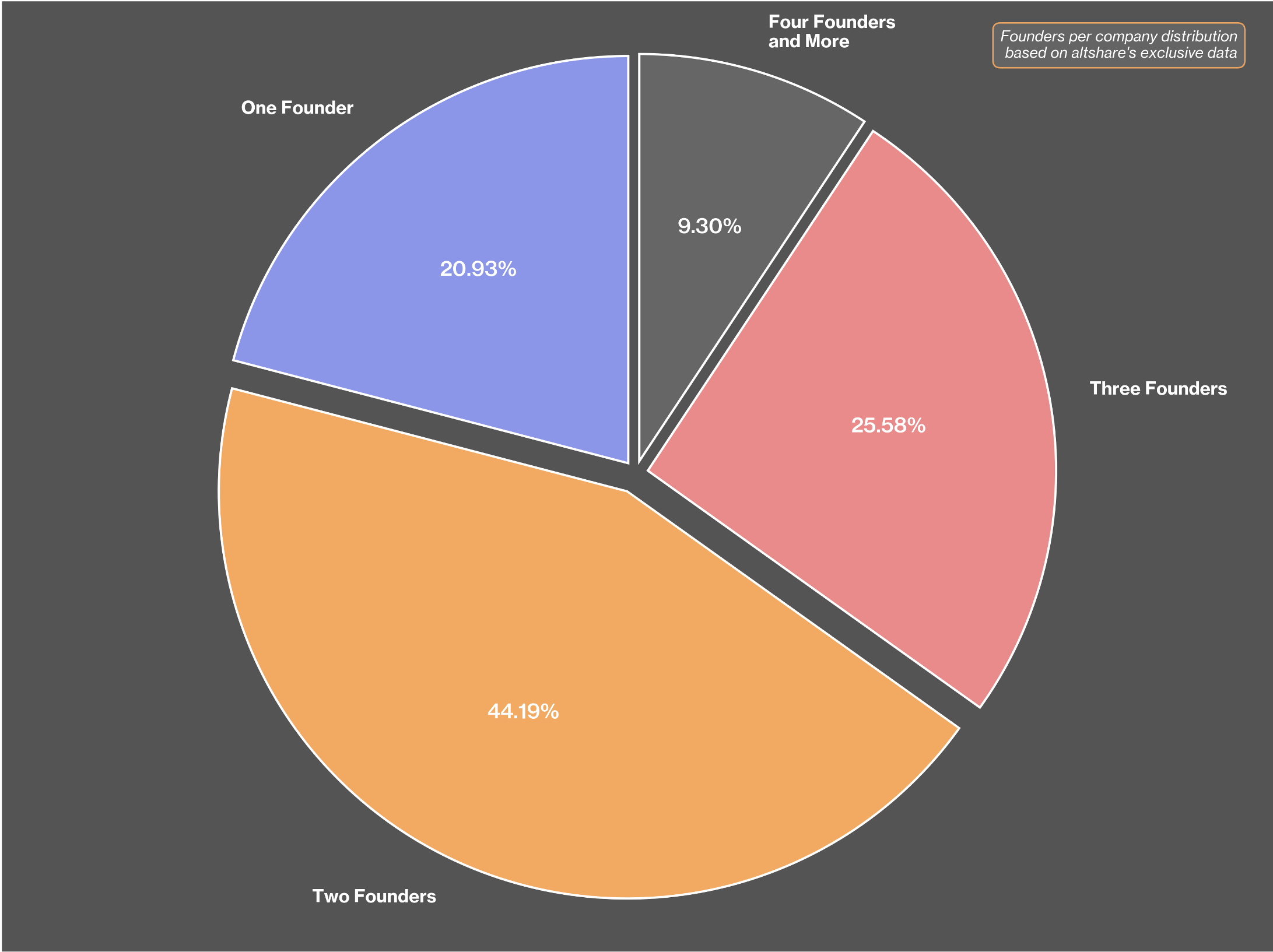

This pie chart shows how companies are divided by the number of founders. The most common setup is two founders, making up about 44% of the sample. Single-founder teams represent 21%, and three-founder teams account for 26%. Companies with four or more founders are rare, at just over 9%.

This matches industry trends, where two or three person teams are preferred for their mix of skills and quick decisions, while larger teams can face coordination issues.

Overall, the data supports the idea that "two is the magic number" for co-founders in early- and growth-stage startups.

Over the past two and a half years, early-stage private tech company valuations have shifted significantly. Since H2 2022, AI-related valuations surged as startups branded themselves as “AI-native” despite limited maturity. This trend was fueled by global investor enthusiasm for LLMs, prioritizing narratives over performance. Cybersecurity valuations rose due to increasing digital threats amid geopolitical tensions.

In contrast, HealthTech saw valuation drops in 2023 post-COVID, but rebounded in 2024 due to AI-assisted diagnostics. FinTech valuations improved gradually after a 2022 low from macro tightening and regulatory pressures, aided by AI-enabled underwriting and fraud detection.

Overall, while AI and Cyber valuations soared, HealthTech and FinTech began regaining attention with more cautious risk premiums.

Changes in Time to Liquidity (TTL) represents the anticipated duration until a startup achieves an exit event, which allows for the conversion of equity into cash for both investors and founders.

In this analysis, "No Change" indicates that the startups have maintained the same TTL expectation year-over-year. This suggests that these companies have not made substantial progress toward their projected exit, effectively postponing their timeline by one year.

A "Decreased" TTL denotes that startups have reduced their expected duration, signaling meaningful progress toward their anticipated exit timeline. This indicates that these companies are moving closer to achieving liquidity as initially planned.

Conversely, an "Increase" in TTL indicates that startups have extended their expected timeline. This typically reflects challenges or delays that have pushed their anticipated exit further into the future.

After a static period from 2023 to 2024, the first half of 2025 is bringing renewed optimism for startups.

Many are now reporting shorter times to liquidity, showing improved operational momentum and a clearer focus on exit strategies. This shift reflects market recovery and increased internal confidence.

At the same time, some companies are extending their timelines, often due to a thorough reassessment of their strategies, growth rates, or commercial expectations.

Together, these trends highlight a more dynamic market where founders are navigating liquidity paths based on real progress and evolving maturity, rather than just external pressures.

About altshare

altshare is a leading, fast-growing Equity Management & Compensation Plans Administration solutions provider. We love challenges. We are obsessed with our clients. We are on a mission to redefine the way founders do equity. All our products & services are supported through the altshare Platform - the only equity management platform built for entrepreneurs.