This report is issued by and on behalf of altshare Ltd. ("altshare") for informational purposes only and shall not be construed as legal, financial, or tax advice.

The information contained in this report is based on data provided to and/or prepared by altshare for its clients. The report is based on an aggregated and anonymized data from altshare's clients.

While this report may address potential legal, financial, and/or tax matters, it does not constitute professional advice in these areas. The opinions or conclusions expressed herein are not to be attributed to altshare. We strongly recommend that you seek the counsel of qualified advisors before taking any actions based on the information provided in this report.

For the avoidance of doubt, altshare shall not assume any liability for, nor be held responsible for any damages, losses, claims, or expenses, whether direct, indirect, incidental, consequential, special, or punitive, arising from the use or reliance on the information contained in this report. altshare shall not be liable for any actions

taken or not taken based on the information contained herein.

altshare does not warrant the accuracy, completeness, or reliability of the data presented and assumes no responsibility for any errors or omissions. The information provided in this report is subject to change without notice.

This report is provided "as is" and altshare disclaims any responsibility for the outcomes of decisions made by the recipient or any third party in reliance on its contents.

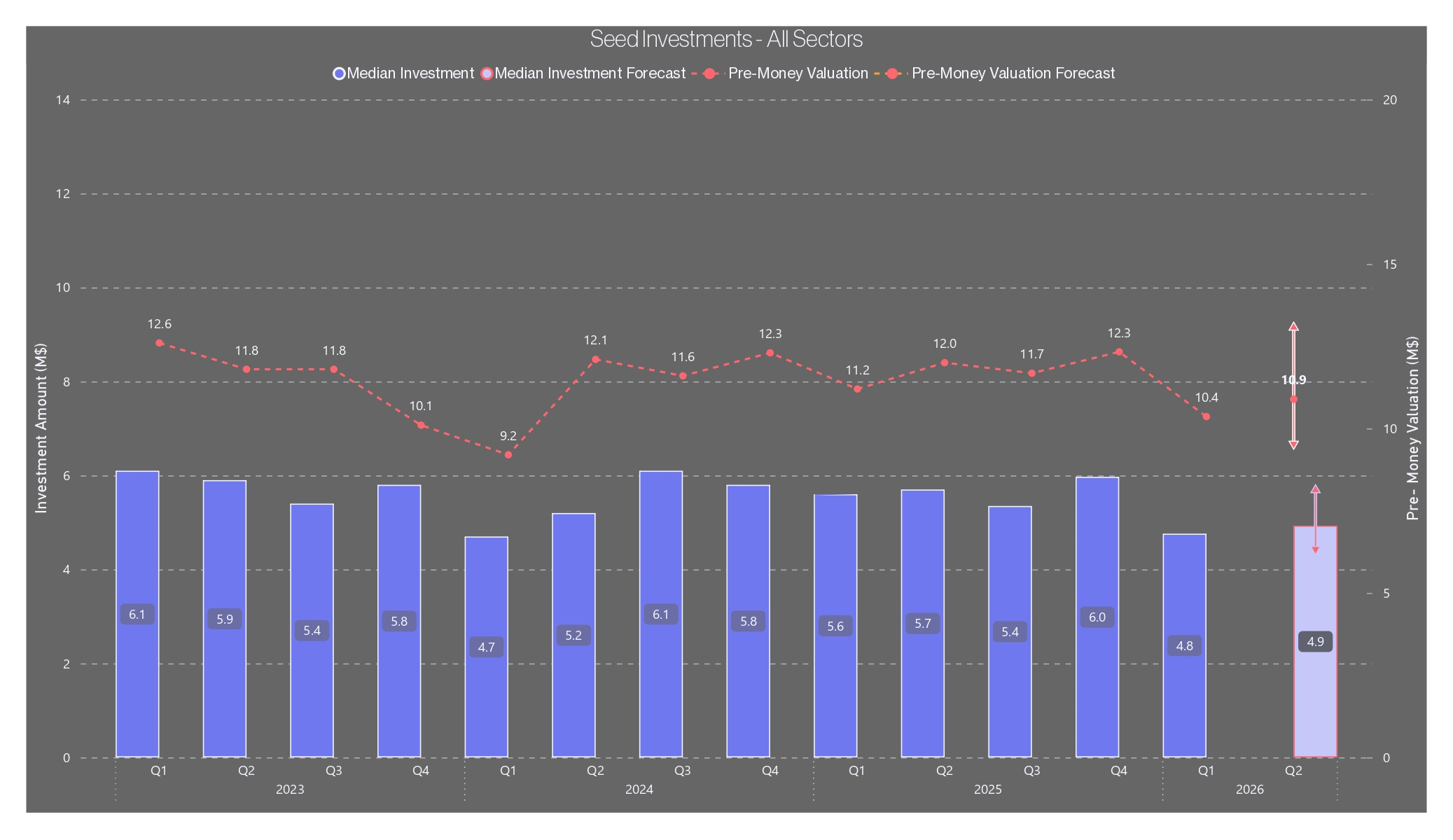

Seed activity paused in Q1 2026, with median investment at $4.8M and pre-money valuation at $10.4M - landing at the lower bound of our forecast range. This marks a reset following a strong Q4, consistent with prior cycles, with the pullback comparable in magnitude to the Q1 2024 dip.

Looking ahead, stabilization is likely in Q2, with median investment edging to $4.9M and pre-money valuation recovering to $10.9M, though geopolitical risk adds near-term uncertainty.

AI cooled in Q1 2026 after peaking in Q4 at $6.5M and $16.4M, but remains structurally strong. Q1 landed at $4.9M and $13.8M - within our prior forecast range, following four quarters of uninterrupted growth.

Our model projects a partial recovery in Q2 2026 to $5.1M and $14.9M. Demand remains strong, but now sharply selective.

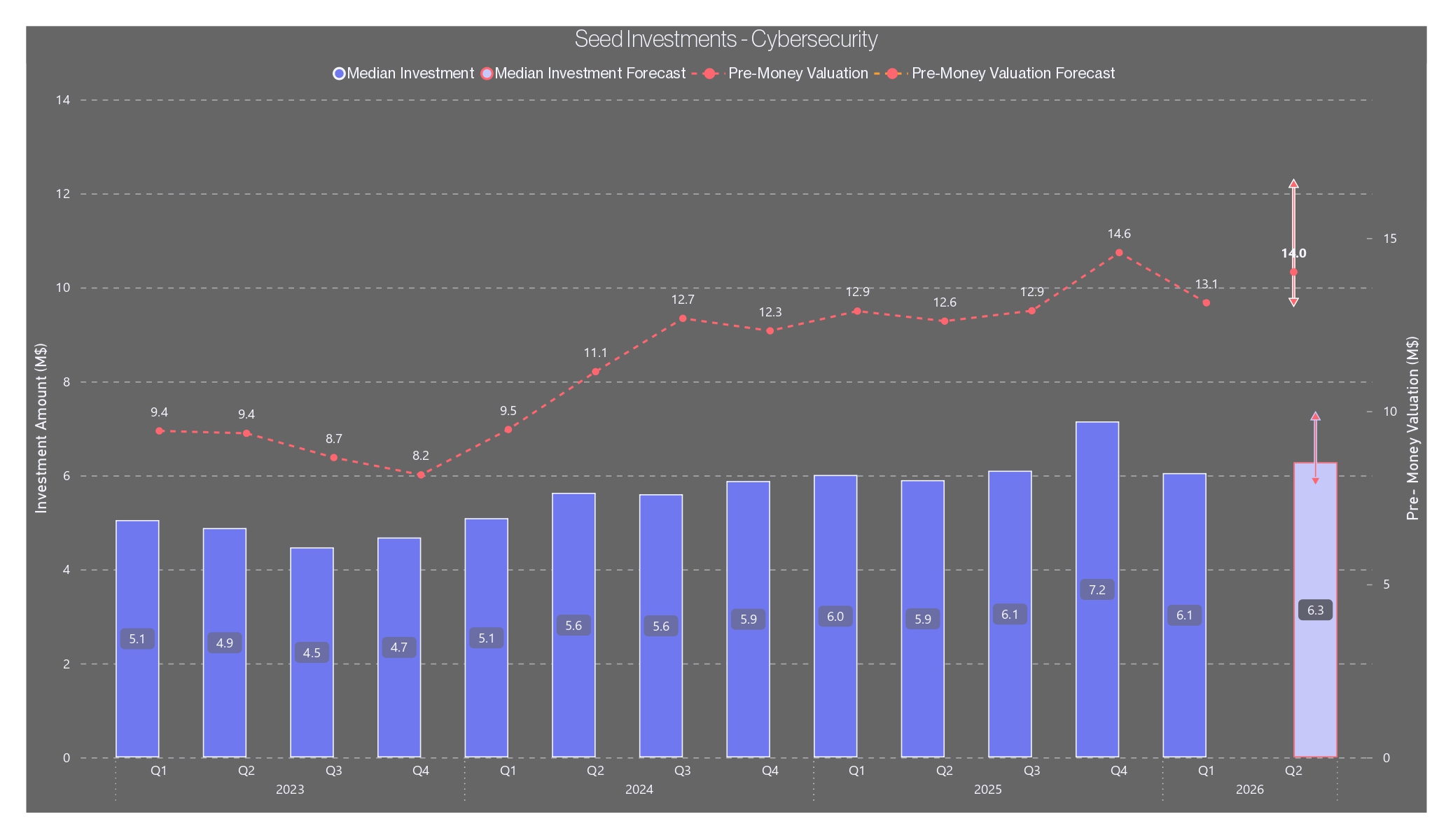

Cyber pulled back from a strong Q4 2025 ($7.2M investment, $14.6M pre-money) to $6.1M and $13.1M in Q1 2026, but remains well above baseline, driven by sustained enterprise demand and expanding threat surfaces.

Our model forecasts Q2 2026 at $6.3M and $14.0M. Geopolitical tension is reinforcing Cyber's strategic relevance, supporting near-term demand.

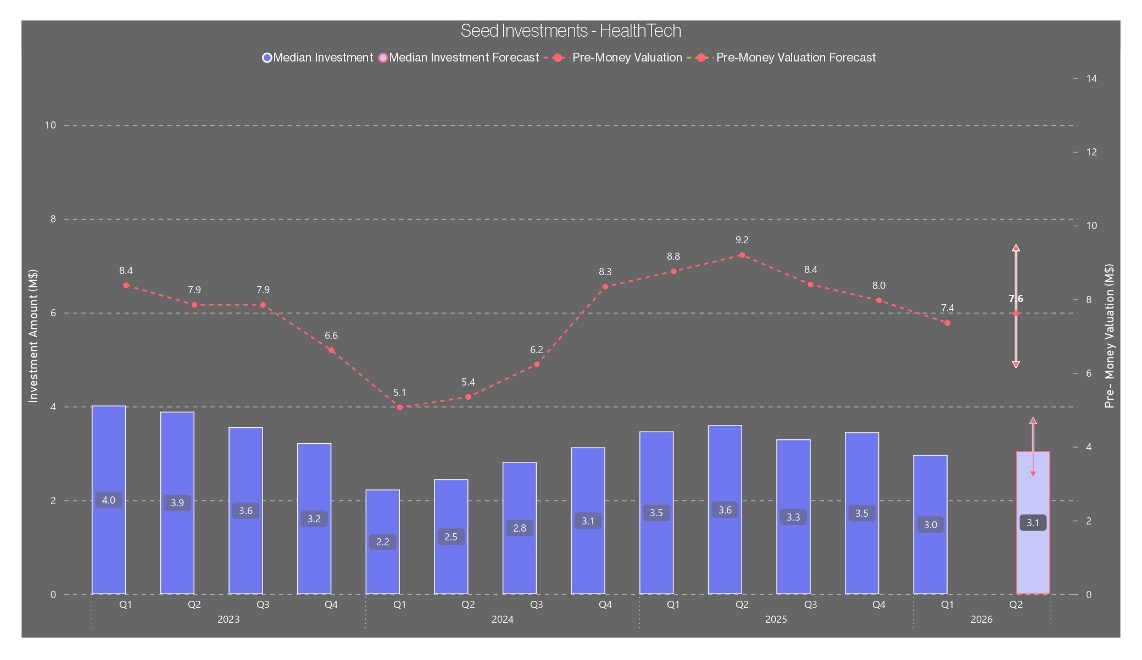

HealthTech continues to move on its own timeline, slower but steady, with Q1 2026 at $3.0M in median investment and $7.4M in pre-money valuation.

It remains the smallest category by round size, by design, not weakness, reflecting longer development timelines and narrower investor pools at the earliest stage.

Our model projects a modest uptick in Q2 2026 to $3.1M and $7.6M. HealthTech is driven by milestones, not market cycles.

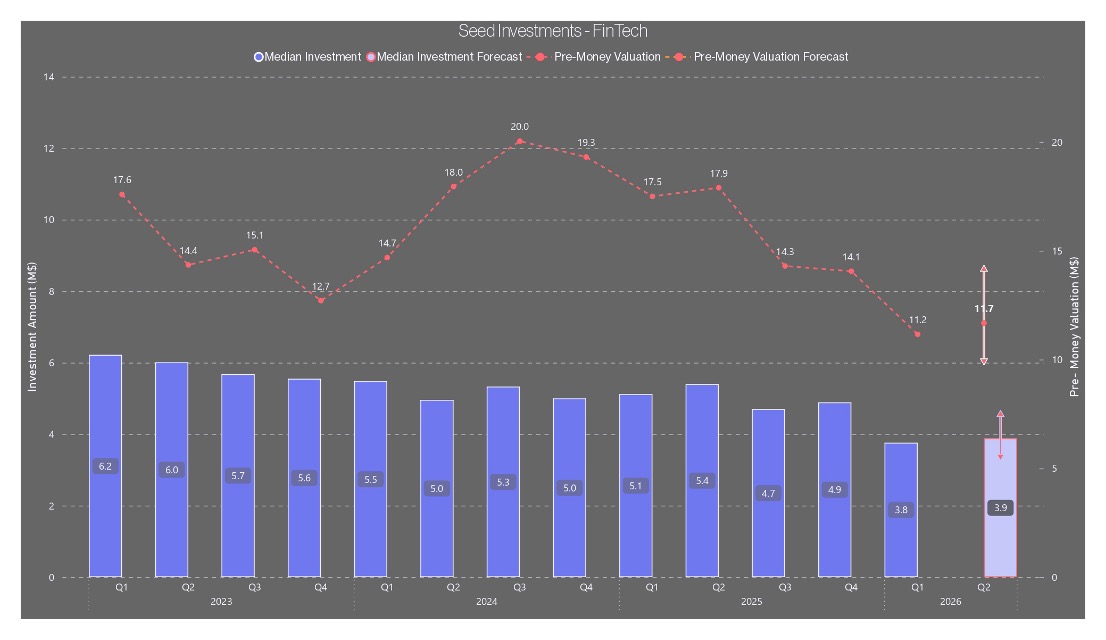

Fintech continues to lose momentum, now at dataset lows, with Q1 2026 at $3.8M in median investment and $11.2M in pre-money valuation. Capital is rotating away, toward AI and defense-adjacent sectors.

Our model projects a flat Q2 2026 at $3.9M and $11.7M. Recovery will require either macro tailwinds or a breakout category.

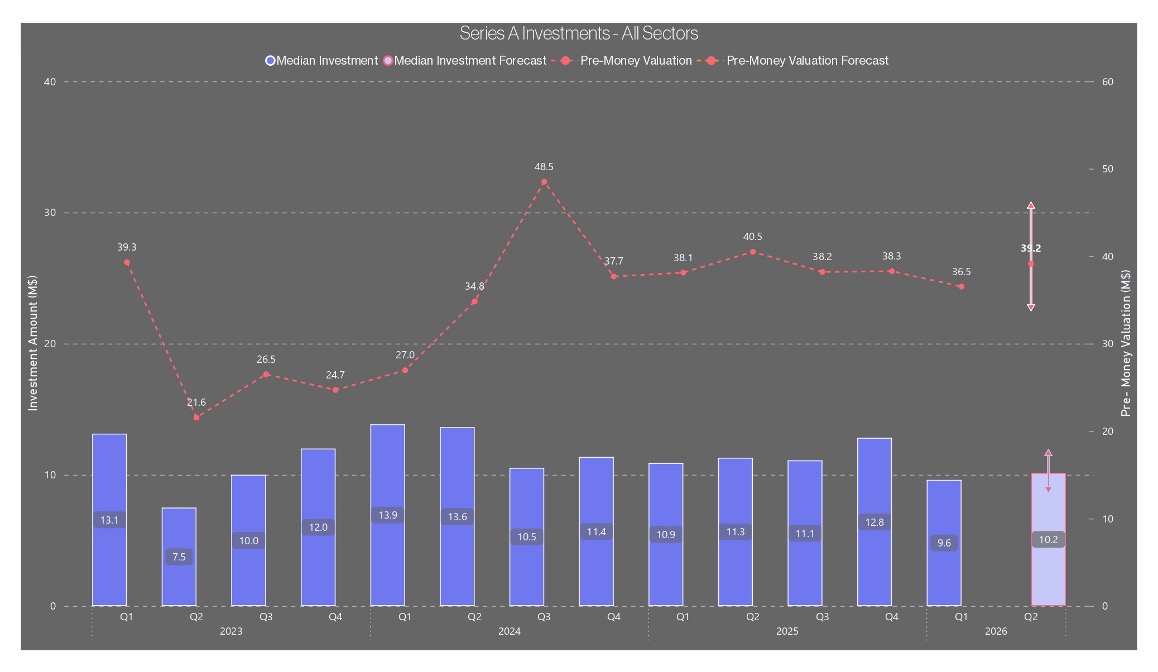

Series A reset in Q1 2026, mirroring the pullback at Seed, with median investment at $9.6M and pre-money valuation at $36.5M - down from $12.8M and $38.3M in Q4 2025. Risk-off sentiment has now fully reached Series A.

Our model projects Q2 2026 at $10.2M investment with pre-money easing further to $35.2M, suggesting investors are compressing valuations even as median round sizes begin to stabilize.

Progression from Seed to Series A is becoming more selective.

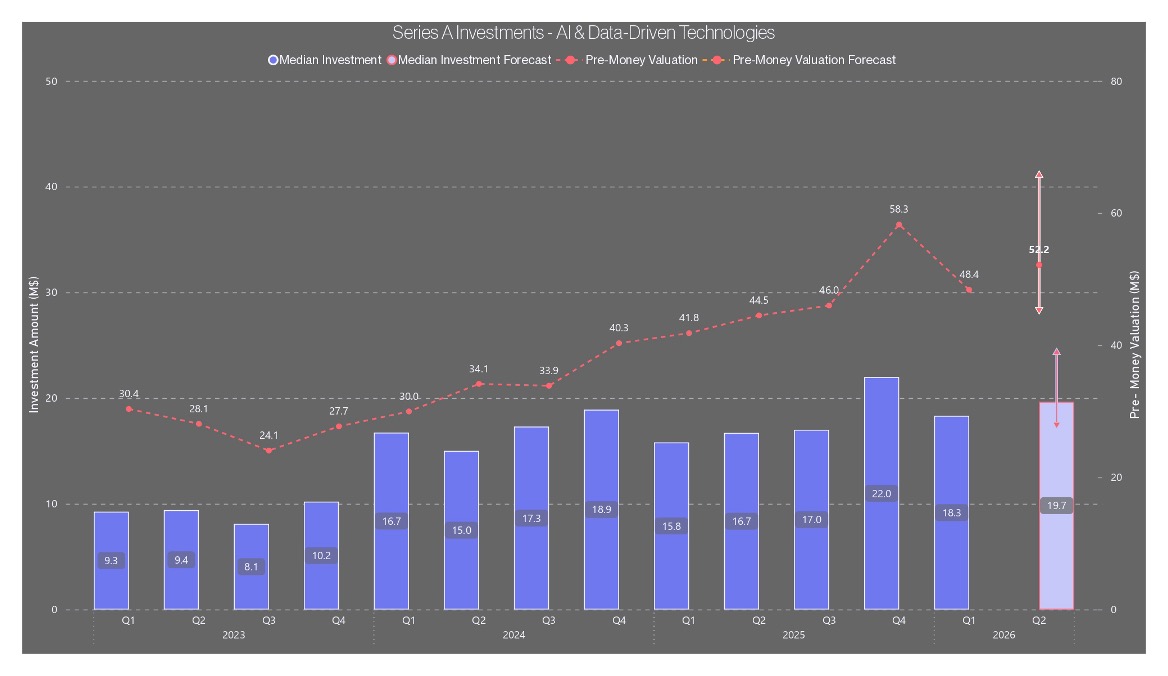

AI corrected but remains the premium category, with Q1 2026 median investment at $18.3M and pre-money at $48.4M - after Q4 2025 hit a record $22.0M and $58.3M. Q4 marked the peak of an 18-month climb in AI Series A pricing; Q1 is normalization, not reversal.

Our model projects Q2 2026 at $19.7M and $51.2M, with a wide confidence range reflecting high outcome dispersion.

Premium pricing remains, but only for proven teams.

Cyber saw the sharpest contraction in capital, but not in valuation - median investment fell 29% to $14.2M in Q1 2026 from $19.9M in Q4 2025, while pre money valuations held firm at $75.2M.

Capital is tighter, but pricing remains intact.

Our model projects Q2 2026 at $14.7M and $78.9M. Rising threat levels continue to support demand.

HealthTech remains the most stable sector in Q1 2026, with median investment at $4.2M and pre-money at $20.1M - a modest step down from Q4 2025's $4.8M and $21.3M.

Movement remains limited, by design.

Our model projects Q2 2026 at $4.3M and $21.2M, essentially returning to recent averages. A low-volatility allocation in an otherwise volatile market.

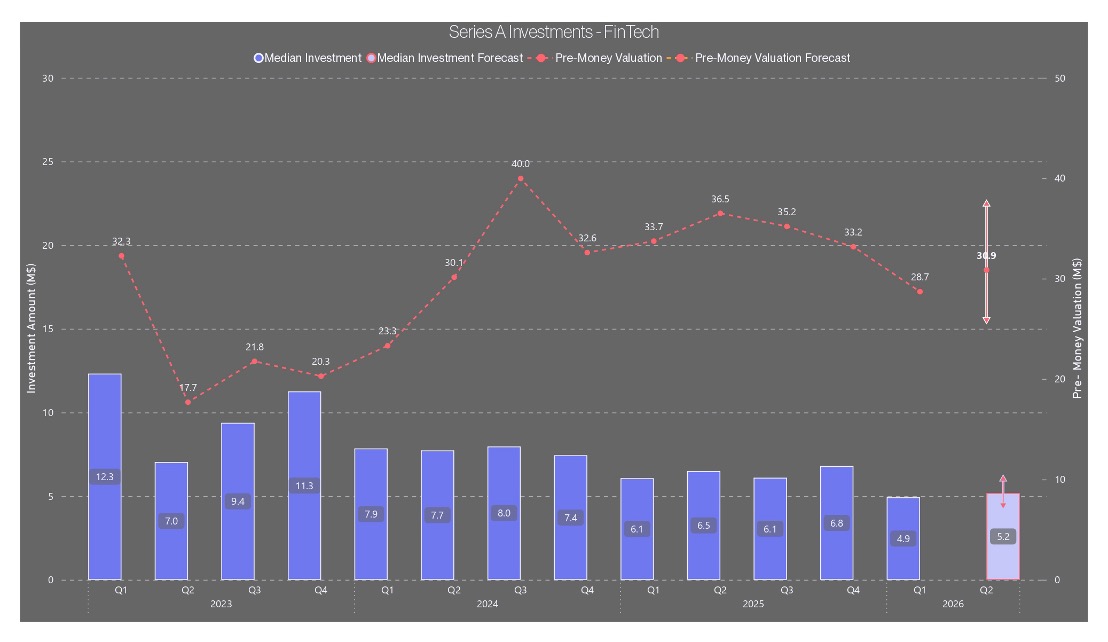

Fintech continues to contract, across both pricing and capital, with Q1 2026 recording the lowest median investment in the dataset at $4.9M. Pre-money valuation fell to $28.7M, well below the 2025 average of ~$34.7M. Fundraising conditions remain structurally challenging.

Our model projects Q2 2026 at $5.2M and $30.9M - a marginal

improvement. No clear inflection point yet.

The pause played out as expected, but selectivity has tightened further. Across both Seed and Series A, median investment and pre-money valuations pulled back, landing in the lower bound of our forecast ranges. The correction was broad-based but uneven - AI and Cyber retreated from strong Q4 peaks while remaining structurally elevated,

whereas Fintech hit its lowest levels in the dataset at both stages. HealthTech proved the most resilient sector, barely moving. The Iran conflict has introduced a new layer of near-term uncertainty but has also sharpened the strategic case for defense-adjacent investment, particularly in Cyber. Our models project stabilization in Q2, though the pace of recovery hinges on how the geopolitical landscape evolves.

The pause played out as expected, but the filter has tightened further. Capital is concentrating, around fewer, stronger companies. Investors are doubling down on defensible positions: strong unit economics, operational discipline, and strategic relevance.

The Iran conflict is not freezing deal flow - it is reshaping it. Defense-adjacent sectors are gaining urgency, while others face longer timelines and harder conversations. The bar continues to rise. Execution and timing now determine who raises and at what price.

The K-shaped recovery is now fully visible in the data. AI and Cyber remain the premium-priced segments at both Seed and Series A, even after their Q1 pullbacks.

Fintech and HealthTech continue to lag, with Fintech in particular hitting dataset lows at both stages. The geopolitical backdrop is adding a new dimension to the divide - sectors with defense and national-security relevance are structurally advantaged in the current environment. For investors: premium persists at the top, opportunity widens below.

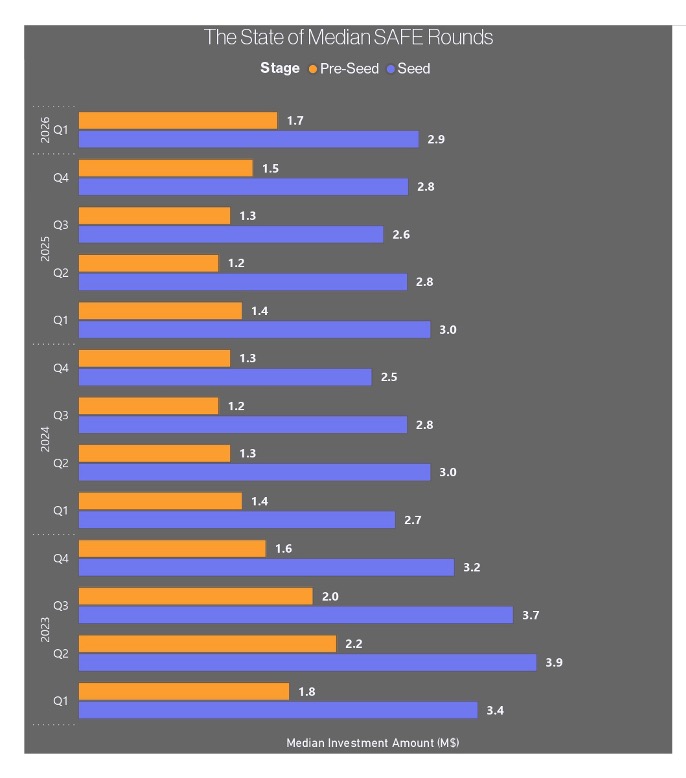

Founders are raising earlier and larger. Pre-seed rounds rose to $1.7M - the highest level since Q1 2023 - after holding within a narrow $1.2M–$1.5M band for nearly two years. Seed rounds edged to $2.9M, in line with their recent $2.5M–$3.0M range.

Notably, the typical step-up from pre-seed to seed has compressed slightly, from roughly 1.9x last quarter to 1.7x, as pre-seed rounds are expanding faster than seed.

This suggests founders are extending runway ahead of a more selective Seed market.

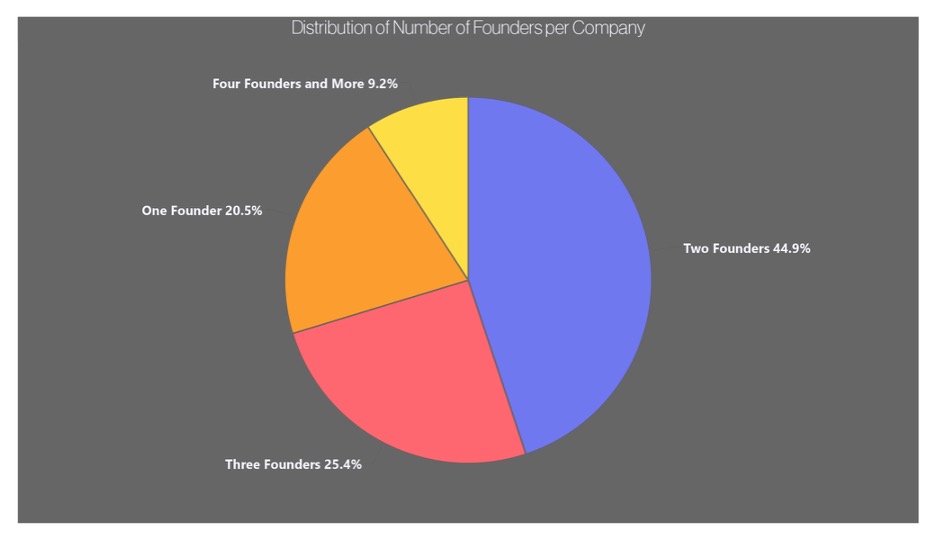

Small teams dominate, two to three founders in ~70% of cases, with two- founder teams alone accounting for 44.9% of the dataset. Solo founders represent a meaningful but smaller share at 20.5%, while teams of four or more remain rare at 9.2%.

Smaller teams consistently outperform on alignment and execution - large enough to cover core functions like product, engineering, and go-to- market, yet small enough to maintain clearer decision-making.

This structure also tends to support more balanced equity outcomes than either solo founders or larger groups.

Most dilution happens early, before founders fully realize it. Founders enter at a median 88.4% ownership at pre-seed and see the sharpest dilution at the Seed stage, dropping to 50.2%. From there, ownership declines more gradually - 39.8% at Series A, 30.1% at B, and 24.1% at C. Employee option pools follow the inverse trajectory, rising from 5.4% at pre-seed to 9.8% at Seed, then expanding incrementally to 12.7% by Series C.

The biggest dilution event is the pre-seed to seed transition, and larger option pools established early tend to reduce the need for disruptive refreshes later. After Seed, both ownership decline and pool expansion follow a steadier, more predictable path.

Multiples are stable, but differentiation is increasing, with sector-level shifts telling a more nuanced story. AI continues to lead at 5.2x, though the slight dip from 5.4x in H2 2025 marks its first decline after a steady two-year climb.

Cyber is closing the gap with AI at the top - now at 5.1x, nearly at parity, as heightened threat environments and expanding enterprise budgets support premium pricing.

FinTech eased to 4.1x from 4.2x, consistent with the broader pressure visible across its investment and valuation data. HealthTech, by contrast, continued

its slow but unbroken ascent to 3.8x, reinforcing its role as the steadiest - if most modestly valued - segment.

The market is pricing with conviction, not momentum. The narrowing gap between AI and Cyber at the top, and the persistent discount on FinTech and

HealthTech, mirror the same selectivity patterns observed in the deal data.

Liquidity is returning, but on stricter terms. One-year delays, which became the default outcome in the 2023–2024 cycle at 78.75%, have steadily declined -

dropping to 57.5% in 2024–2025 and further to 53.5% in the 2025–2026 (Q1) window. Meanwhile, the share of companies exiting as planned has climbed to

36.7%, the highest level in the dataset, up from just 12.5% at the trough.

Confidence is returning, but selectively. That said, multi-year delays have edged up slightly to 9.8%. A subset of companies is still choosing to wait for stronger

scale or a more compelling exit environment - a pattern that may intensify given the current geopolitical uncertainty.

About altshare

altshare is a leading, fast-growing Equity Management & Compensation Plans Administration solutions provider. We love challenges. We are obsessed with our clients. We are on a mission to redefine the way founders do equity. All our products & services are supported through the altshare Platform - the only equity management platform built for entrepreneurs.